By S.N. Misra

06 Aug , 2016

The Kargil Conflict had fortuitously brought to the centre-stage the need for an integrated approach towards intelligence gathering and joint operations. The 26//11 Mumbai attack has woken us to the reality of a unified approach between the states, the Coast Guard and the Indian Navy. The Defence Procurement Procedures over the years have tried to bring transparency into our procurement process and there have been some moves towards increasing private sector participation in defence manufacturing. However, unlike the automotives and telecom sector, the relationship between the DPSUs, the DRDO and the private sector remain uneasy and adversarial. The DPSUs still do not consider the private sector as partners but as contractors. The record of private sector players such as L&T in strategic programmes like that of Arihant is salutary. A defence capability improvement would need major structural change. Either we have a DGA-like structure or the COCO structure of the USA with the government providing oversight on strategic issues.

The Kargil Conflict had fortuitously brought to the centre-stage the need for an integrated approach towards intelligence gathering and joint operations. The 26//11 Mumbai attack has woken us to the reality of a unified approach between the states, the Coast Guard and the Indian Navy. The Defence Procurement Procedures over the years have tried to bring transparency into our procurement process and there have been some moves towards increasing private sector participation in defence manufacturing. However, unlike the automotives and telecom sector, the relationship between the DPSUs, the DRDO and the private sector remain uneasy and adversarial. The DPSUs still do not consider the private sector as partners but as contractors. The record of private sector players such as L&T in strategic programmes like that of Arihant is salutary. A defence capability improvement would need major structural change. Either we have a DGA-like structure or the COCO structure of the USA with the government providing oversight on strategic issues.

The Kargil War uncovered the fault lines in the coordination between different agencies which are engaged in containing external threats…

The Kargil War uncovered the fault lines in the coordination between different agencies which are engaged in containing external threats. The Group of Ministers Recommendations (2002) made wide-ranging recommendations to fill up this critical void by providing for an Integrated Defence Services (IDS) Structure, Joint Services operation and creation of an Acquisition Wing. The DPP 2002 was the first definitive document which dealt with the nuances of acquisition by categorising our defence requirements as ‘Buy’ (Import) and ‘Buy and Make’.

The winds of liberalisation wafted through the defence sector (2001) when DPSU monopoly was jettisoned by allowing the private sector to participate fully in defence equipment manufacturing. The foreign Original Equipment Manufacturers (OEMs) were also allowed to bring in Foreign Direct Investment (FDI) up to 26 per cent. DPP 2005 witnessed significant changes by bringing in a ‘Make’ category, and offset provision to leverage our big ticket acquisition to lure foreign suppliers to provide key technology and FDI. DPP 2013 encouraged private sector shipyards to compete for orders for surveillance vessels.

Presently, the Transfer of Technology arrangement provides India the ‘know-how’ rather than the ‘know-why’…

After the UPA government moved into the saddle, the ‘Make in India’ policy has assumed centre-stage by promoting 25 identified sectors. Budget 2015-2016 increased the FDI limit in defence to 49 per cent and the MSME sector financing is being facilitated through the Mudra Bank initiative. In this backdrop, a committee under Dhirendra Singh has given extensive recommendations on measures to restructure our Defence Procurement Policy with a view to synergise the defence industry base with the ‘Make in India’ momentum.

The Dhirendra Committee Recommendations

The gravamen of the Committee is to bring the defence sector into the cusp of the unprecedented opportunity that the ‘Make in India’ initiative offers by providing an eco-system where design, R&D, manufacturing, maintenance and export capability would thrive. This would require a proper balancing between importation and indigenous manufacturing, keeping in view our low self-reliance index (30 per cent). The committee brings out the fact that India is the largest arms importer.

Table -1below highlights the details of the level of import and sources of procurement of a few countries.

It can be seen from the table-1 that most of the weapons imported by India and China are sourced from Russia, while in case of Pakistan, they are either of Chinese or American origin. Of late, many of the imports by India clearly show a predilection towards the USA and Israel. It would, therefore, be apt to bring up the level of indigenous defence production in our nine DPSUs and 40 ordnance factories.

It can be seen from Table 2 that the average increase in the Value of Production (VOP) of Defence PSUs and the ordnance factories is of the order of ten per cent and they contribute nearly $7 billion to defence acquisition. However, they have sizeable import content, barring the ordnance factories. Most of the Defence PSUs also have a very poor record in terms of value addition.

The Committee has observed that for improving our capability we need to climb up the competence ladder i.e. from system integration to component, design and manufacture to system designed development and manufacture. Presently, the Transfer of Technology arrangement provides India the ‘know-how’ rather than the ‘know-why’ resulting in a situation where even for the upgrades, DPSUs such as HAL depend on the collaborator. A case in point is the SU 30 upgrade.

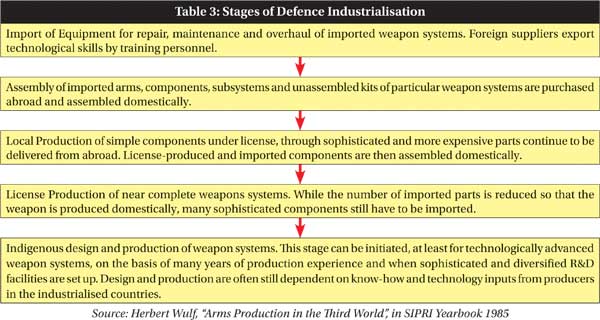

Professor Herbert Wulf while examining the process of defence industry capability in developing countries has identified five major stages through which these countries travel to achieve a high modicum in defence industry capability.

The following table brings out the stages:

{kind=link}

It can be seen from the above flowchart that India is still in the fourth stage. To transit to the last stage we would have to move out from the role of an assembler to that of a value adder where the IPR rights reside with India.

Increasing Indigenous Content

The major thrust of the Dhirendra Committee report is to improve indigenous capability by promoting ‘Buy in India’ and ‘Buy and Make (India)’ option where the indigenous content is sought to be improved from the present level of 30 per cent and 50 per cent (DPP 2013) to 40 per cent and 60 per cent respectively.

The following table would bring out their recommendations with regard to categorisation:

The report gives primacy to ‘Buy (India) Indigenous Designed Developed Manufacturing (IDDM)’. The real difficulty, however, would be how to prioritise between ‘Buy and Make’ (through the Defence PSUs) or and ‘Buy and Make (India)’ where there would be competition for technology transfer between Defence PSUs and the private sector.

A case in point is the ‘Make in India’ initiative for the manufacture of the Kamov helicopter in India where Reliance Industry was bidding for technology transfer from Russia, while the government has opted for HAL. The report suggests strategic partnership models with the private sector as a concept and has referred to US and French investment models where strategic partnership factors in issues such as risk sharing and risk rewards. It also places its thrust on MSMEs, who should be treated on a par with the large corporate organisations. It calls for eschewing suspicion by quoting Mahatma Gandhi, “The moment there is a suspicion about a person’s motive, everything he does becomes tainted.”

It would be interesting to note that the Kelkar committee had strongly recommended that the government should identify a few large corporates such as the Tatas, L&T, Mahindra & Mahindra to be called Raksha Utpadan Ratnas who should be given equal opportunity in the matter of production and integration of major weapons and platforms as the DPSUs. The Dhirendra Committee skirts this suggestion.

DPP 2016

The Defence Minister seems to have gone completely by the recommendations of the above Committee and DPP 2016 reflects the unbridled optimism on ‘Make in India’. It has given first preference to ‘Buy (Indian)’ (IDDM) with 40 per cent indigenous content and ‘Buy (India)’ as the second preference with a 60 per cent indigenous content. ‘Buy and Make (India)’ and ‘Buy and Make’ have been given third and fourth preference. The ‘Make’ category will operate either in isolation or in tandem with the above four types of acquisition options.

The Defence Minister seems to have gone completely by the recommendations of the above Committee and DPP 2016 reflects the unbridled optimism on ‘Make in India’. It has given first preference to ‘Buy (Indian)’ (IDDM) with 40 per cent indigenous content and ‘Buy (India)’ as the second preference with a 60 per cent indigenous content. ‘Buy and Make (India)’ and ‘Buy and Make’ have been given third and fourth preference. The ‘Make’ category will operate either in isolation or in tandem with the above four types of acquisition options.

Procurement is the highway along which the armed forces would like to have a smooth ride on the broad back of the Indian industry…

The DPP 2016 has taken a dim view of the offset provision as it observes that such a stipulation increases the acquisition cost by 14 to 18 per cent. It has accordingly increased the threshold limit to Rs 2,000 crore as against the earlier Rs 300 crore. In ship building procedures, there are two categories – one from defence shipyards and the other through competitive tendering. However, it does not clarify whether frigates and submarines would be offered to the private sector for competitive bidding. Presently, only manufacturing of surveillance vessels such as IPV, OPV are open to such competitions and the orders have been invariably bagged by the private sector, with much better delivery compliance and economy in cost. The DPP, however, has left the chapter on strategic partnership blank.

Concerns In Manufacturing

Procurement is the highway along which the armed forces would like to have a smooth ride on the broad back of the Indian industry in partnership with OEMs and reputed design houses. The NDA government is making a spirited foray into this manufacturing highway with the JAM trinity as a powerful force multiplier. The New Manufacturing Policy envisaged creating 100 million jobs during the next decade besides improving our share of manufacturing from 16 to 25 per cent. This would require effective participation of the MSMEs (15.8 lakh units) who engage nearly 85 per cent of the unorganised employed. The experience of major global manufacturing countries such as Germany, Japan, South Korea and China reveals that they have invested handsomely on skilled set valued synergy with SMEs and they believe in economies of scale as the following global comparison would highlight.

It can, therefore, be seen that besides lack of economy of scale, we suffer from the missing middle. It is heartening that the Dhirendra Committee has recommended that in the ‘Make’ category 90 per cent funding of the prototypes of values of up to Rs 10 crore should be reserved for the MSME sector.

The critical element for success of defence manufacturing would, however, devolve on skilling, R&D and improving factor productivity of which was highlighted by Professor Robert Solow, the Nobel Laureate, in his equation Y=A X Kα x Lβ (where Y is the output, A is scale of production & level of technology, K & L are factors of production and α & β are factor efficiencies).

Suggestions to build strategic partnership for building platform and weapon systems fails to take note of the serious capability gap of the DRDO…

Structural Concerns

The Sisodia Committee had suggested that the DGA model of France where design, development, production, acquisition and post production maintenance is driven by a composite organisation, should be adopted in India. This would require political will as organisations such as the DRDO do not want to be part of such an accountable composite set up. One of the reasons why Russia has been extremely successful as a defence manufacturing hub is because the Research Agency comes under the Production Organisation and works in tandem. The Rama Rao committee, in the context of the failure of the Kaveri engine for the LCA programme, had also endorsed this viewpoint. In the USA, defence manufacturing is on the basis of Contractor Owned Contact Operated (COCO) model as against the Government Owned Government Operated (GOGO) model in India. Therefore, without fundamental structural changes, the Department of Defence Production would be perceived as favouring the DPSUs and OFs.

Critical Technology

Suggestions to build strategic partnership for building platform and weapon systems fails to take note of the serious capability gap of the DRDO in terms of material, weapons, sensors and propulsion systems. Neither NAL Bangalore nor DRDO has come up with credible indigenous alternatives for the carbon fibres which are required for the production of our ALHs. We have to willy nilly depend on Japan for this.

In the case of air-to-air missiles, the DRDO is yet to come up with the reliable ASTRA alternative. The communication sets (TADIRAN) for Tank regiments from Israel are yet to be replaced by DRDO’s CNR radio. The Akash missile designed by DRDO is now being given up by all the services due to its performance deficit. Almost every engine in every propulsion system used by the Indian Navy is being sourced from the USA.

The global synergy that we are seeking through the ‘Make in India’ slogan is stymied by the FDI policy…

In case of the IAF, it is either from Russia or from USA. In the case of tanks, they are either from Russia or Germany (MBT). As regards the sensors, we are struggling big time in developing a Focal Plane Array, AESA Radar, Ring Laser Gyro and Passive seekers. It is indeed a sad commentary that our dependence on foreign sources for weapons, sensors and propulsion for major platforms is almost 100 per cent. It is, therefore, surprising that the Committee is so sanguine about indigenous R&D bolstering defence industry capability through Buy (India) (IDDM) option, when our design capability for critical subsystems is so palpably inadequate.

The Way Forward

The Kargil Conflict had fortuitously brought to the centre-stage the need for an integrated approach towards intelligence gathering and joint operations. The 26//11 Mumbai attack has woken us to the reality of a unified approach between the states, the Coast Guard and the Indian Navy.

The Defence Procurement Procedures over the years have tried to bring transparency into our procurement process and there have been some moves towards increasing private sector participation in defence manufacturing. However, unlike the automotives and telecom sectors, the relationship between the DPSUs, the DRDO and the private sector remains uneasy and adversarial.

DPP 2016 is high on rhetoric and weak in terms of the fundamental structural changes needed to transit from Build to Design (TOT) to Design to Build (MAKE)…

The DPSUs still do not consider the private sector as partners, but as contractors. The record of private sector players such as L&T in strategic programmes like that of Arihant is salutary. A defence capability improvement would need major structural change. Either we have a DGA-like structure or the COCO structure of the USA with the government providing oversight on strategic issues.

It is unfortunate that the offset policy is being given a short shrift without taking stock of its global success in countries like Brazil which has developed the Embraer aircraft through the offset provision. The design capabilities of the DRDO, HAL and BEL remain weak. The global synergy that we are seeking through the ‘Make in India’ slogan is stymied by the FDI policy in defence which does not encourage the OEMs and design houses to invest in India on a long term basis.

The very fact that only $5 million has come in through FDI in defence and Rs 56 lakh after increase in FDI cap to 49 per cent is commentary enough on our shortsighted FDI policy. DPP 2016 is high on rhetoric and weak in terms of the fundamental structural changes needed to transit from Build to Design (TOT) to Design to Build (MAKE).

© Copyright 2016 Indian Defence Review

No comments:

Post a Comment