Introduction

Less than a decade after weathering massive geo-political upheavals from the Arab Springs, the Middle East is on the verge of yet another crisis; the plummeting price of crude oil. “Rentier states” in the Middle East, have for several decades, secured their status-quo by building an overwhelming portion of their economy dedicated to the sale of crude oil.[i] While the rentier system has been successful in propping up Middle Eastern governments for decades, the downside to this system is the economic and political uncertainty created by the rapidly changing value in a single commodity.[ii] With an anticipated drop in the price of crude oil, the recent stability of the Middle East is likely to become vulnerable as governments begin to experience a significant economic downturn.

Background

The term “rentier state” comes from the sale of “rents”, or single commodities, established to fuel a state’s economy and overall political structure.[iii] For example, a form of universal basic income exists in Kuwait; while this placates the middle class and prevents upheaval, it is only made possible through the sale of massive amounts of its country’s natural resources.[iv] Conventional wisdom suggests the primary recipients of these consequences will be the oil exporting countries such as Saudi Arabia, the UAE, and Kuwait. However, non-rentier states such as Jordan and Egypt find themselves at large risk for upheaval as well; oil profits from rentier states have been subsidizing major parts of the economies of neighboring nations in order to foster alliances and stability.[v] Thus, an oil crisis is set to affect not just rentier countries, but virtually the entirety of the Middle East. The purpose of this project is to analyze the consequences of a possible permanent drop in oil prices, and the possible follow-on effects to the stability of Middle Eastern governments. It is important to note that the Middle East isn’t just facing an immediate crisis from the immediate drop in prices, instead it is a long term problem that will take decades to return from.

Methodology

This paper examines the likelihood of conflict in a given nation caused by falling oil prices. First, a correlation between falling oil prices and instability are determined by examining trending data analysis. Second, in order to determine how negative economic factors can contribute to political instability the Human Development Index (HDI) is measured against political instability, coupled with the GDP per capita being measured against the likelihood of conflict in a given area. Third, the estimated value of crude oil is determined from available open source data on projected oil values. Fourth, case studies of the UAE and Egypt are used to predict likely real-world outcomes based on previous trends from both Gulf and non-Gulf states in the Middle East. Finally, anticipated long-term impacts, consequences of falling value, and preventative measures provide an outline for progress moving forward.

Human Development vs Political Instability

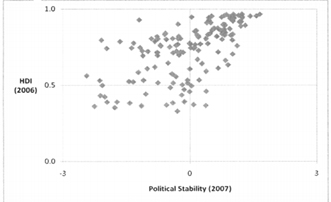

The World Bank’s Human Development Index (HDI) is a collection of data used to track overall progress of a nation regarding the welfare of its people. It combines life expectancy, education, per capita income, etc., to give an overall picture of a nation’s health. Political stability is an index calculated by several factors that affect a governments ability to “effectively formulate and implement sound policies”[vi] Figure 1 outlines the positive correlation between stability and HDI, as well as the inverse; lower levels of political stability correlates positively with a lower HDI.[vii] In other words, countries that face instability in their governments are more likely to suffer on a larger scale. Figure 1 supports the theory that a given event in the Middle East that may disrupt governments will likely reverberate on large scale crises across the region.

Figure 1: Political Stability and Human Development Index for all countries

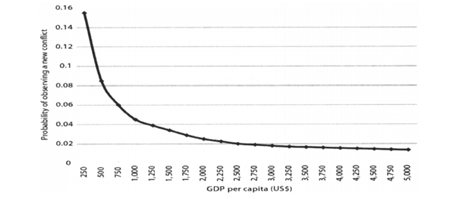

GDP per Capita vs Likelihood of Conflict

Figure 2: GDP per Capita and the probability of observing a new conflict

Past vs Future Crude Oil Values

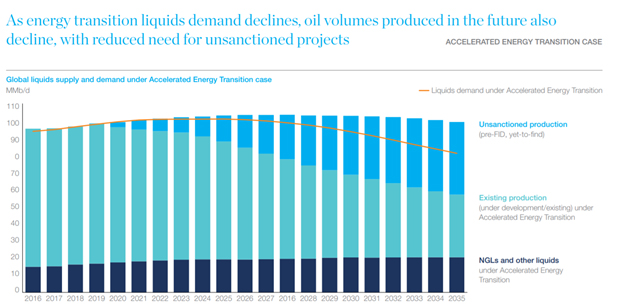

Crude oil value is expected to decline steadily over the next several decades. The two main factors are an increase in supply due to future efficiency in extraction methods, as well as the increase in reliance on alternative energy.[xi] The United States’ success in hydrolic fracturing extraction, otherwise known as “fracking” has led the U.S. Department of Energy to claim that by 2035 45% of the United States gas consumption will be via fracked oil.[xii] Likewise, the McCinsy Institute, experts in global economic projections, argue that by 2035 alternative clean energy sources (not including fracking) will make up nearly half of all energy demand worldwide.[xiii] Figure 3 displays the anticipated decrease in demand for liquid energy (crude oil) through 2035.[xiv] Consequently, a significant increase in oil supply combined with a decrease in oil demand will likely lead to a slow and steady decline in oil value through at least 2050.[xv]

Crude oil value is expected to decline steadily over the next several decades. The two main factors are an increase in supply due to future efficiency in extraction methods, as well as the increase in reliance on alternative energy.[xi] The United States’ success in hydrolic fracturing extraction, otherwise known as “fracking” has led the U.S. Department of Energy to claim that by 2035 45% of the United States gas consumption will be via fracked oil.[xii] Likewise, the McCinsy Institute, experts in global economic projections, argue that by 2035 alternative clean energy sources (not including fracking) will make up nearly half of all energy demand worldwide.[xiii] Figure 3 displays the anticipated decrease in demand for liquid energy (crude oil) through 2035.[xiv] Consequently, a significant increase in oil supply combined with a decrease in oil demand will likely lead to a slow and steady decline in oil value through at least 2050.[xv]

Figure 3: Global Liquids supply and demand under Accelerated Energy Transition case

Case Studies

United Arab Emirates

The United Arab Emirates provides a good blueprint for Gulf nations moving forward. Despite initially constructing their economy around their sale of crude oil, the UAE has since recognized this weakness, and is currently making attempts at wider economic diversification. The United Arab Emirates have long avoided political instability by ensuring its citizens have their needs met via a robust welfare system. [xvi]Over 90% of employed Emiratis work for the government, and subsidies for people’s normal expensive affairs, such as marriage, are often paid for by the government.[xvii] However, this system is only possible through the massive profits generated by the UAE’s exportation of crude oil. In addition, the UAE’s homogeny in its economy means even a relatively slight dip in oil prices could threaten their entire country with recession. To the UAE’s credit, they have made significant efforts in the past decade to diversify their economy in an attempt to lessen the devastation caused by falling oil value. The now famous tourist landmarks that dot the landscape of Abu Dhabi are a clear example of their attempts to lean into other industries.[xviii] While hedging its bets on tourism certainly isn’t the perfect solution, the UAE has at least identified the need to branch out into other industries. Major oil exporting countries in the Middle East would be wise to follow the UAE’s lead in economic diversification if they wish to increase their chances of stability in the future.

Egypt

Egypt faces a more difficult future with no clear economic reform plan. While oil exporting gulf states must prepare for an incoming economic recession, non-exporting countries should fear for their stability as well. Nations on friendly terms with OPEC often receive large grants and subsidies in order to keep their own economies afloat during turbulent times.[xix] During the turn of the century, on average, 10% of Egypt’s GDP came from Gulf state grants and remittances. Following extreme political instability from 2011-2015, OPEC nations sent billions in aid to Egypt for the explicit purpose of ensuring the stability of the government.[xx] While Egypt doesn’t have the economic power to mimic the UAE’s welfare system, it does still depend largely on subsidies to its citizens to guarantee compliance. However, the risk of reduction of these subsidizes has plagued stability in Egypt for the past decade. In April of 2019 the government announced a new cut to fuel subsidies, citing poor economic development as the culprit.[xxi] Experts fear this recent cut will only contribute to the unstable situation Egypt has found itself since the Arab Spring began.[xxii] Gulf countries facing major economic recession will likely slash foreign aid to non-exporting countries such as Egypt, which in turn, could affect the stability of the entire Middle East.

Impact

Several sectors of Middle Eastern society require reform in avoid long term consequences. While extreme economic reform is necessary, success in the future will ultimately hinge on each country’s ability to adapt politically as well. Preventing collapse after oil falls cannot be singularly accomplished through investment diversity. A fall in oil will affect not just the economy, but the overall social contract governments have held with their people for nearly a century. Certain steps, such as privatization, attracting foreign investment, and integrating into the global economy can only be achieved if political transparency rises and political corruption falls.[xxiii] Breaking of social contracts has already caused major problems in the region. Tunisia, Egypt, Syria, and Yemen have all seen revolutions and civil wars this past decade, in large part due to its citizenry losing trust in their government. According to the Corruption Percentage Index (PCI) developed by Transparency International, Middle Eastern governments ranked among the world’s lowest in terms of transparency for the past decade.[xxiv]

The recent 2019 attacks on Abqaiq and Khurais oil facilities in Saudi Arabia point to major weaknesses in the security of Saudi Arabia’s oil infrastructure. The attacks reduced the country’s oil output by nearly half that day, dropping the entire world’s supply by 5%.[xxv] The Houthi-led attack displayed a new dynamic in which to fight in the Middle East; by attacking economic infrastructure. Historically, guerilla attacks in the Middle East tended to target political, military, or social targets. This recent attack is significant to future developments because it displays not only the effectiveness of attacking economic infrastructure, but also the security weaknesses of these targets. Rentier states now need to diversify not only due to future dropping oil prices, but also for short term economic reasons as well. If attacking oil refineries continues to be effective, more attacks should be expected in the future. Likewise, if attacks continue, oil markets can become extremely volatile until security issues are resolved. Regardless of whether it jumps or dips, an overall volatile market is a death sentence for rentier states; lack of economic diversification combined with an unpredictable market will drive away foreign investment. Foreign investment is key to allowing rentier states to diversify. Until Saudi Arabia (and all OPEC states) can strengthen security of their facilities to the point where attacks are no longer effective, their ability to attract foreign investment and by extension, pull themselves out of their rentier economic cycle, will continue to decline.

Long term foreign investment is dependent on a given nation’s ability to persuade shareholders that political turbulence is unlikely to occur. Likewise, successful privatization of industries is dependent on international corporations having high trust and confidence in the reigning government to not drastically change the dynamic of their country.[xxvi] A significant reduction in political corruption, and an increase in political transparency is necessary in countries that wish to join the international economy on a level outside of oil exportation.

Conclusion

Ever since the discovery of oil in the Middle East in the mid-20th century, the region has relied heavily on rentier government systems to secure their stability.[xxvii] However, this system has always precariously depended on the value of a single natural resource in order to prevent total collapse. While rentier systems are prone to economic swings, unemployment is another major concern. Oil extraction and exportation requires such little personnel employment that a massive percentage of Gulf nations need to provide for their citizens via an extensive welfare system. These welfare systems in turn are only made possible through the profits generated from oil. A long-term shortage of profits means governments will no longer be able to placate their citizens with money, and unemployment will start to emerge as a major concern. Given this foundation, falling oil value could threaten to unravel the social contract between Middle Eastern citizenry and their governments. Doing so will likely lead to a major increase in political stability, which in turn could lead to major crises throughout the region. If Middle Eastern countries wish to see a way out of this trajectory, they should look to the example set by the UAE for economic diversification by investing in new industries. However, major economic reforms are only possible if governments reform politically in conjunction. Corruption and political turmoil turn away foreign investors, and thus, any chance at joining the global economy.[xxviii] The Middle East can wade through this incoming crisis, but major economic and political reforms are necessary first. Failure to do so could create extreme large-scale problems in the Middle East, perpetuating the cycle of poor development in the region.

Addendum

The recent 2019 attacks on Saudi Arabia’s oil facilities required an update to this essay, given their relevance to the subject and the impacts they will have on the region. As of September 17, 2019, the date of this essay, there are still details emerging regarding the attacks. As of this writing, the Houthi rebels have claimed responsibility for the attacks, however, no evidence yet exists to the public that can definitively point to the source. The United States claimed Iran is responsible, France claims they have seen no evidence of responsibility from anyone yet, Iran denies involvement, and the Houthi rebels have claimed responsibility.[xxix] There is some evidence to suggest the point of origin of the strike may be near Iraq or Iran, but no definitive perpetrator can be proven as of this writing.[xxx] Regardless, theorizing who is responsible has no effect on the significance it holds to this essay. While details are still emerging, the fact remains that the recent attacks certainly display a weakness in OPEC security, and display a new dynamic by which to attack these states. For this reason, it was relevant to include under the “Impacts” section of this essay.

No comments:

Post a Comment