Aya Adachi, Alexander Brown, Max J. Zenglein

Key findings

Over the past years, political relations between the EU and China have deteriorated. This has increased the risks associated with economic pressure. A sober assessment of companies’ vulnerabilities is necessary to adjust to this new reality.

Over the past years, political relations between the EU and China have deteriorated. This has increased the risks associated with economic pressure. A sober assessment of companies’ vulnerabilities is necessary to adjust to this new reality.Beijing uses economic coercion for signaling and deterrence. By pressuring prominent companies or sectors, it tries to deter others from crossing certain lines. MERICS identified 123 such cases between February 2010 and March 2022. Fearful of becoming a target, companies might avoid making public statements on sensitive issues or deem it safer to align themselves with the positions and objectives of China’s government.

Since 2018, China has increased its use of economic coercion, and the triggers have become more diverse. China’s red lines have expanded beyond traditional issues of sovereignty and national security to include China’s international image and the treatment of Chinese firms abroad.

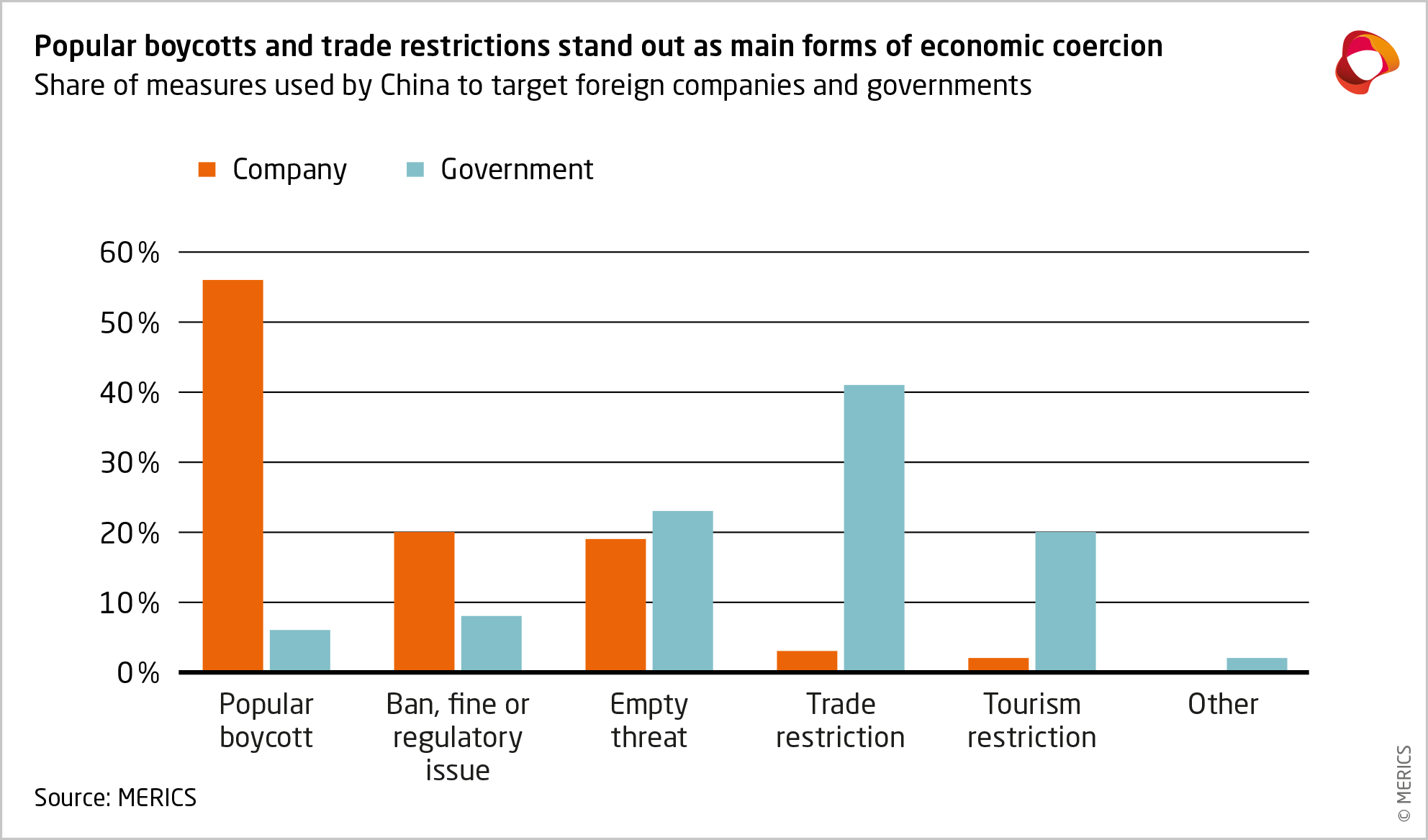

The forms of coercion employed by China include a range of measures. Beijing resorted to popular boycotts in 56 percent of cases when companies crossed a perceived red line. When responding to the actions of foreign governments, China adopted restrictions on trade and tourism in 41 percent and 20 percent of cases, respectively.

Empty threats are another common form of coercion, accounting for about a fifth of all cases (21 percent). Such bluffs can be effective, as selecting a prominent target may work to deter other governments and companies from unwanted actions.

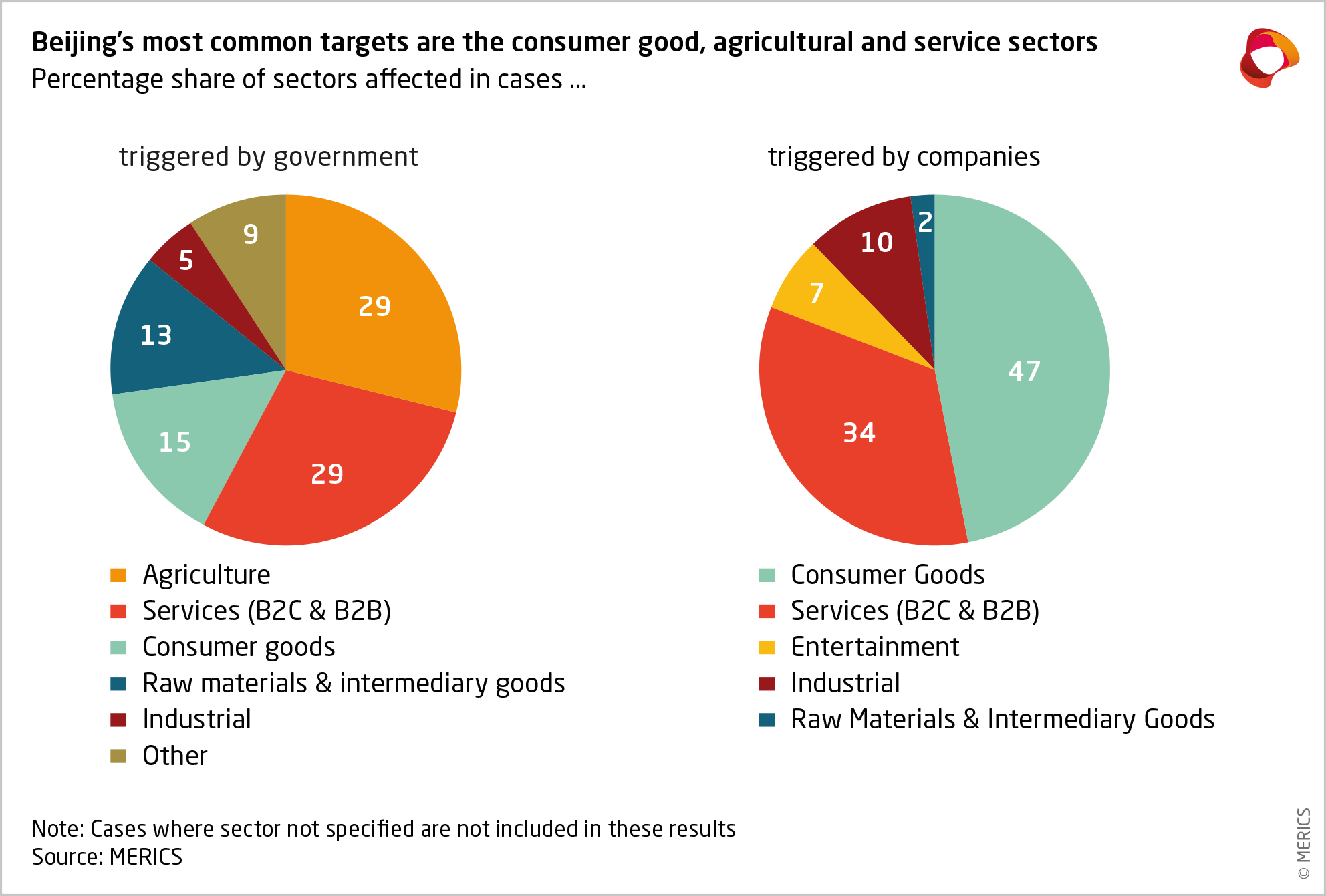

When exerting economic pressure, Beijing makes sure to minimize adverse effects on its own economic development. Companies in the consumer and agricultural goods, commodities and services sector are the most frequent targets of retaliation, since in these areas alternative providers can usually be found. Almost half of recorded coercive measures were in the consumer goods sector.

The most vulnerable sectors and companies are those deemed to be of little value to the strategic goals of central and local governments in China, such as economic and technological development. Where the interests of Chinese competitors clash with foreign firms, then there is additional risk.

Foreign companies of high strategic relevance, such as high-tech firms with a large investment presence in China, are likely to be more secure. Those companies can be outspoken on issues which do not align with the position of China’s government and are unlikely to face severe repercussions.

The examples of companies from Japan, South Korea and Taiwan show how firms of different risk profiles are managing their exposure. Some high-risk companies revert to keeping a low-profile, but companies of all risk types are pursuing diversification and other measures to balance their economic ties with China.

1. Europe is increasingly in China’s crosshairs as the relationship is reset

European business interests in China are becoming more exposed to different forms of Chinese economic retaliation, which follows sometimes their own actions but increasingly also measures taken by the EU or its member states. Quickly escalating disputes with China’s government mean that the risk exposure of European companies to economic coercion is often out of their control. China’s souring relations with Lithuania over the renaming of the Taiwan representative office has been a case in point, with companies operating in Lithuania caught in Beijing’s crosshairs. It has become clear that companies can now have their operations affected by retaliation following the actions of any EU government.

The deepening of economic relations with China is now increasingly seen in the context of growing systemic rivalry – if not conflict. Bridging differences is becoming ever more difficult as the systemic divide is widening. Political risks are on the rise, exposing vulnerabilities in companies’ China business. They will have to adapt to new dimensions of risk.

The EU and its member states have taken more robust stances towards China in recent years, including introducing policies risking confrontation with Beijing over its key interests. This covers political confrontations over human rights or Taiwan as well as economic conflict over issues ranging from subsidies to market access.

China’s leadership nonetheless has a strong incentive to continue prioritizing economic interests and thus accept political differences. However, it might at the same time calculate that its best option is to leverage existing and prospective economic ties to further these interests. Thus, the threat of economic retaliation is a new reality in Europe’s relationship with China. Navigating it will require European companies to properly assess their risk exposure and to prepare steps to mitigate the impact.

Leveraging the fear of economic loss has become a powerful tool for China’s government when dealing with Europe’s recent policy shift. Beijing hopes to influence policy decisions and to shape “correct” views on the relationship by threatening or imposing economic costs. This strategy is already defining the relationship as recent examples of Chinese measures targeting Lithuania over Taiwan or fear of Chinese reactions to banning Huawei as a 5G provider illustrate. While the list of prominent cases of Chinese economic coercion is growing, they are only the tip of the iceberg as many remain unreported.

Exhibit 1

To gain a clearer picture of the nature of China’s increasing use of economic coercion, MERICS has compiled the specifics of publicly known cases from all over the world to deduce patterns in Beijing’s behavior.1 We identified 123 cases between February 2010 and March 2022, with their frequency increasing since 2018 (see Exhibit 1). However, the number of instances when an action was taken by a European actor because it anticipated a measure by China without this actually existing is not captured in the reviewed cases. As such, the effectiveness of China’s use of economic coercion could be significantly higher.

The combination of the informal nature of many Chinese measures and companies’ fear of being affected means that the majority of cases remains invisible. Mindful of their China exposure, companies might not be willing to speak out about economic coercion—including over market access or technology transfer, and even more so political issues—to avoid retaliation. China’s government has tremendous power over how a foreign company can operate in the country. Officials can effectively turn the taps of revenue from the Chinese market on or off at will. As a result, European companies might work hard to water down the positions of governments or business associations towards China, de facto lobbying for China’s interests. China’s most effective form of economic coercion might therefore be covert pressure on companies.

As Europe and China recalibrate their relationship, the potential for economic conflict is likely to increase. European companies will be fearful of being caught in the middle. In a highly dynamic business environment, many risks associated with China might be predictable, but many are not. Either way, economic coercion is now part of the new dynamic risk exposure in economic ties with China. This makes it ever more important for European companies and governments to have a clear picture of the actual economic vulnerabilities. In developing one, the experience of East Asian countries is a rich source of case studies to show which industries and business sectors have been typically targeted and what effective measures were taken to minimize risks while preserving economic interests in China.

Exhibit 2

2. Navigating the triggers of China’s economic coercion and its policy toolbox

Perceived interference in the country’s internal affairs has long defined the “red lines” of China’s government over the past decades. Criticizing China’s human rights situation or undermining the positions of the Chinese Communist Party (CCP) on Taiwan or Tibet have long been triggers for conflict. The list of red lines has gotten somewhat longer but it still mostly involves sovereignty, security and territorial claims (see Exhibit 2). The cases of economic coercion identified indicate that traditional red lines remain the dominant triggers, accounting for 75 percent of them.

The scope of triggers for economic coercion has become more diverse as China’s economic strength has grown. Since 2018, Beijing has more frequently resorted to using its economic leverage to threaten punishment for perceived attacks on its wider interests, including overseas. The greater politicization of economic ties will likely lead to additional new red lines, making it more difficult to anticipate triggers of coercion. In theory, taking any position that is not aligned with that of the CCP is likely to lead to a response. However, whether and how China’s government responds, is harder to predict.

Giving the impression of being thin-skinned about its red lines is part of Beijing’s strategy. It forces foreign firms to tiptoe around sensitive issues by fueling the perception that their business interests are contingent on “correct” behavior. Matters are further complicated by China’s government primarily employing opaque and informal forms of coercion, allowing it to deny that it is resorting to economic pressure, and to deploy and retract measures at will.

The identified cases of economic coercion show that China has six types of measures in its toolbox.Popular boycotts: Foreign consumer goods can become subject to a popular boycott and face a drop in reputation and sales in China. Although such boycotts may appear to be organic expressions of consumer sentiment, they spread over social media platforms that are carefully monitored by government officials and are in some cases spurred on by state media outlets. Thus, any successful popular boycott can be seen as indirectly orchestrated by the government.

Administrative discrimination: Administrative procedures and regulatory checks are often used arbitrarily to coerce a target. In many cases, it is impossible for targeted companies to provide evidence of discriminatory behavior and litigate the case. The deployed measures are highly diverse, including complications with customs processing, exclusion from procurement, one-off fines for “violations,” and labor or safety regulations that can lead to the forced closure of business operations or costs associated with adjustments to meet new requirements.

Empty threats: Threats without any real action can sometimes prompt foreign governments and companies to comply with Beijing’s objectives. China has issued vague warnings of unspecified “consequences” without any follow-up measures on several occasions. Prominent examples include attempts to safeguard Huawei's access to 5G network markets in France, Germany, the United Kingdom, and the United States. In this way, China leverages the fear and uncertainty of foreign actors to apply pressure.

Legal defensive trade measures: In recent years, Beijing has developed several defensive trade policy instruments, including the unreliable entity list, the anti-foreign sanction law, and the export control law. It has also strategically used anti-dumping measures to retaliate against countries like Australia.2 China may adopt more formal methods in the future to limit market access, raise tariffs, or impose other costs.

Trade restrictions: Beijing frequently restricts trade by targeting imports of agricultural goods or commodities. Only on rare occasions has it employed or threatened to employ export restrictions, as was the case with rare earths to Japan in 2010.

Tourism restrictions: In pre-pandemic times China stood out as the country with the largest international tourism expenditure. In 2019, Chinese tourists spent USD 254.6 billion, making up 17 percent of the world total.3 By issuing an official travel warning, reducing visa services, or canceling tour operations, the government can drastically limit the number of Chinese travelers and thus impact the tourism, retail and hospitality industries in a targeted country.

3. Patterns of economic coercion: China seeks to minimize costs to itself through pragmatic target selection

China’s choice of coercive measure differs depending on whether it responds to actions taken by a foreign government or company. Popular boycotts are the tool of choice when targeting companies, accounting for over 50 percent of identified cases, followed by administrative discrimination, which accounts for 20 percent (see Exhibit 3). To target a government, China usually restricts the flow of goods and people to exert broader economic pressure. These two measures account for 61 percent of cases of coercion against foreign governments.4 Empty threats are also frequently employed against both governments and companies and were used in a fifth of all cases.

Exhibit 3

Exhibit 4

Consumer brands and services, including in entertainment and hospitality, are the economic sectors most prone to being targeted (see Exhibit 4). Consumer goods are more susceptible to popular boycotts and import bans. The same applies to imported commodities (including energy and raw materials) and agricultural goods (including food and beverages) that are associated with a particular country rather than a company (for example, wine or coal from Australia). Commodities and agricultural goods account for 18 percent of all cases. Producers of industrial or manufactured goods ranging from vehicles to machinery and electrical components are less likely to be targeted and make up 10 percent of cases.

The architects of China’s economic coercion are pragmatic when selecting targets. Beijing’s application of economic pressure to date reveals the following four patterns.Strategically relevant companies are not targeted. China employs economic coercion to promote its national interests. It is willing to bear the cost of economic inefficiencies or trade diversion as part of this process but it will not undermine its core goals for economic development and industrial upgrading. As a result, it rarely targets foreign companies in strategic industries that bring key technologies, intermediary products, or significant investment into the country.

Sectors with abundant substitutes are vulnerable. To minimize the impact of economic coercion on local business and consumers, China’s government tends to restrict market access for products and services for which there are abundant substitutes at home or abroad. The typical target sectors of agriculture, consumer goods, and tourism fit this approach very well. By the same token, the government avoids going after products where dependencies exist.

China uses economic restrictions to support local firms. Where possible, China will hit two birds with one stone by inflicting pain on a target company or sector while in the process furthering its own strategic goals or satisfying domestic interests. Nationalist boycotts are an effective way to stimulate the consumption of local brands and boost domestic industry. Lobbying by domestic corporate interest groups can also influence the selection of targets.

China uses empty threats to influence behavior without incurring costs. At times China will bluff when a red line is crossed but the matter does not warrant action that could further damage bilateral relations or disrupt business activities. As long as a few precedents of action exist, such threats can be effective, and selecting a prominent target can send a strong signal to apply pressure on governments and companies alike. Instances where China issued a warning but did not clearly implement a follow-up measure account for 21 percent of cases.

4. East Asian companies respond to perceived risks from China

China’s neighbors in Asia are the countries most affected by the opportunities and challenges of its economic and political rise. Japan, South Korea, and Taiwan are particularly exposed to a rapidly changing China due to their geographic proximity, economic interdependence, and growing political and security tensions with the country.

Over the past two decades, economic ties have deepened while at the same time these countries have been targeted by economic coercion. As China grew economically stronger and politically more assertive, tensions rose frequently during the 2000s, and Beijing has repeatedly applied economic coercion to deal with political disagreements. Japan, South Korea, and Taiwan (JKT) make up about 25 percent of the identified cases. For these neighbors, tensions are a fundamental part of their relationship with China despite their deep economic integration. Looking at their experience offers valuable lessons for dealing with the threat of China’s economic coercion.

Exhibit 5

Exhibit 6

Having a large reliance on China does not automatically translate into vulnerability to economic pressure for a company. The JKT countries’ experience of Chinese economic coercion is in line with the broader triggers and patterns discussed in the previous section. For them, China’s actions were always triggered over its traditional red lines. This is in contrast to cases in the EU and the United Kingdom where economic interests were threatened for excluding Huawei from 5G networks. This was not the case in JKT countries despite their governments having done the same. Human rights issues are far less prominent if not absent in JKT countries’ business relations with China. The most common sectors in these countries targeted by economic coercion were agriculture, consumer products, entertainment, and tourism. High-tech sectors with a heavy investment footprint in China including those providing imported intermediate inputs needed for final production in the country were off-limits, given the potential negative consequences for the development of the Chinese economy.

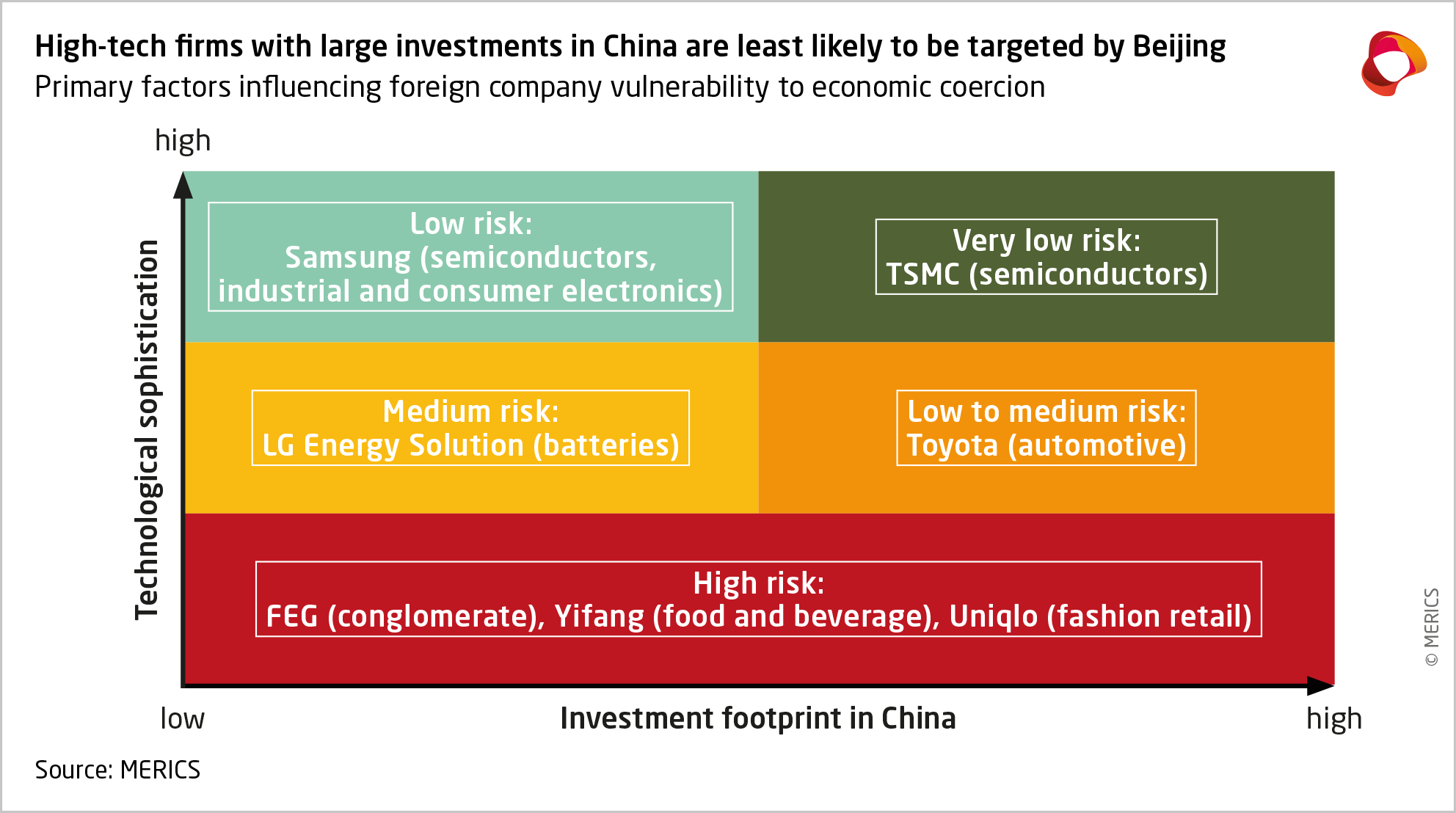

Based on these patterns, the primary factors that determine a company’s risk profile when it comes to economic coercion is the mix of its technological sophistication and investment footprint in China (see Exhibit 6). Below are examples of JKT companies from each risk profile, including ones that have experienced economic coercion and ones that have successfully managed to avoid being targeted despite having large business interests in China. These examples show how companies responded to coercion or the perceived risk of it.

Samsung (South Korea – Semiconductors, industrial and consumer electronics)

What happened: After Samsung listed China, Taiwan and Hong Kong as separate countries and regions, Chinese K-pop star Lay Zhang canceled his brand ambassadorship with the company in 2019.5 But, in contrast to other companies that were fined or boycotted for similar reasons, Samsung was able to avoid further consequences.

Pattern: The Samsung case shows how Beijing is less willing to exert strong pressure against a company that provides critical technology.

Response: DiversificationSamsung has taken precautionary measures by reducing its production exposure to China. Reports show that Samsung halted production in the country of smartphones in 2019 and of computers in 2020, with only two semiconductor manufacturing sites left in Suzhou and Xi’an.6

These decisions to shift production are broadly considered to have been driven by rising labor costs, increasing trade tensions between the United States and China, and the rising risk perception surrounding Chinese supply chains.7

Toyota (Japan – Automotive)

What happened: In 2012, Japan’s government nationalized the Senkaku/Diaoyu islands that previously had been privately owned. The measure resulted in nationwide anti-Japanese protests in China as well as strikes and temporary production halts at Toyota manufacturing plants and a drop in car sales.

Pattern: Despite being among the top foreign investors in China, Toyota is not entirely safe from being targeted as it is one among many car manufacturers in the country and alternative products are available.

Response: Safeguarding China business and diversificationBetween 2013 and 2021, the China share of Toyota sales and production rose from 10.4 to 20.2 percent and from 9.7 to 19.2 percent respectively.8 China was Toyota’s second-largest market and second-largest production base.

There is little evidence of a shift in Toyota’s production strategy after the 2012 anti-Japanese protests, as its China share of total production in Asia increased from 12.4 percent in 2012 to 29.6 percent in 2021.

Toyota is exploring ways to reduce its dependence on materials controlled by China. In 2018, the company unveiled a new kind of magnet that cuts its use of rare-earth elements by about half.9

LG Energy Solution (South Korea – Batteries)

What happened: LG Energy Solution has been among the targets of coercion triggered by the security altercation between China and South Korea over the latter’s deployment of a US Terminal High Altitude Area Defense (THAAD) system in 2017.10 Beijing responded by excluding Chinese electric vehicle (EV) makers using battery packs supplied by South Korean makers from subsidies schemes. Consequently, Chinese battery manufacturers CATL and BYD made strong gains in market share at the expense of their South Korean competitors.

Pattern: The case of LG Energy Solution represents an example of China hitting two birds with one stone, by using coercion to support domestic firms.

Response: DiversificationDespite no longer being able to compete in the Chinese market, LG Energy Solution still holds a significant global market share in EV batteries at 21.5 percent.11 In 2021, the company reported an increase of 42 percent in revenue from 2020 and a 4.3 percent increase in operating profits from the previous year.12 However, China’s CATL has taken the lead with a global market share of 32.5 percent.

LG Energy Solution has set up 50:50 joint ventures with General Motors and Geely, and it has recently announced that it plans to invest around USD 5.5 billion in 2022 to construct and expand its battery production plants in China and the United States.13

Far Eastern Group (Taiwan – Conglomerate)

What happened: During the 2020 elections, Far Eastern Group (FEG), one of Taiwan’s biggest conglomerates, donated NTD 58 million to the Democratic Progressive Party, which interprets the status quo over Taiwan as de facto independence. Beijing responded by fining FEG CNY 36.5 million (USD 5.72 million) on various grounds, from tax to fire safety.14

Pattern: The case of FEG is an example of a company with a high-risk profile as its products (including building materials and synthetic fibers) are easily replaceable for the Chinese economy.

Response: Safeguarding China business and diversificationAfter the fines were issued, FEG’s chairman, Douglas Hsu, responded by apologizing and saying that he “opposes Taiwanese independence” and “like most Taiwanese, I hope cross-strait relations maintain the status quo.”15

FEG has taken some steps to limit its high exposure to the Chinese market by expanding its reach into Southeast Asia and North America.16

Yifang Fruit Tea (Taiwan – Food and beverage services)

What happened: After the Taiwanese beverage maker Yifang Fruit Tea closed down one of its branches in Hong Kong for a day in solidarity with protestors in August 2019, calls for a popular boycott of the company quickly emerged in China and also spread to other bubble tea brands.17

Pattern: As a visible, low-end consumer brand highly exposed to the Chinese market with plenty of competitors, Yifang exemplifies a company at risk of suffering from a popular boycott.

Response: Safeguarding China business and diversificationYifang publicly supported Beijing’s “one country, two systems” stance and denounced labor strikes in Hong Kong (which resulted in a counter backlash and boycotts and the closure of more than 30 Yifang shops in Taiwan).18 Bubble tea brands HeyTea and Gong Cha also affirmed their support for Beijing in the hope of distancing themselves from the backlash in China.19

Since the incident in 2019, Yifang has expanded to Cambodia, Canada, Dubai, France, the Philippines, Sweden, Thailand, and the United States. Other Taiwanese bubble tea brands also expanded outside China.20

Companies that avoided being targeted:

TSMC (Taiwan – Semiconductors)

No known measures or threats have been levied against TSMC due to its crucial position in the global value chain for semiconductors. Given its role in turning Chinese chip designs into finished products and that it has two production facilities in Nanjing and Shanghai, acting against it could severely hurt China’s ambitions to enhance the competitiveness of its chip industry.21

Response: DiversificationTSMC’s recent announcement that it will invest substantially in manufacturing factories in Japan and the United States has been widely interpreted as a shift away from China, justified mainly by recent political tensions and the higher perceived risk of an armed invasion of Taiwan.22 The China share of the company’s revenues has declined sharply; having hovered above 17 percent between 2018 and 2020, it fell to 10 percent in 2021.

TSMC’s measures are far from a full decoupling of activities on the mainland and linkages still run deep. There are also reports of a USD 2.8 billion investment by TSMC in its manufacturing plants in Nanjing.23

Uniqlo (Japan – Fashion retail)

Uniqlo walks a tightrope to avoid choosing between China and the United States. It joined the Better Cotton Initiative in 2018 but has refrained from taking a position regarding human rights violations in Xinjiang, in contrast to other international apparel manufacturers which came under heavy scrutiny in 2021.24

Response: Doubling down on China Even after the United States barred Xinjiang cotton products, including Uniqlo imports in January 2021 due to allegations the company had sourced cotton from there, Fast Retailing (Uniqlo’s parent company) maintained its position with a carefully crafted statement.25 26 While competitors faced losses in China revenue ranging from 20 to 38 percent in November 2021, for speaking out against the human rights situation in Xinjiang, Uniqlo avoided boycotts and only experienced a drop of 0.9 percent in the same month.27

Rather than limiting its exposure to the Chinese market, Uniqlo aims to double down on its benefits, leveraging its unique selling point of offering functional apparel using so-called high-tech fabrics that thus far have proved difficult to copy for Chinese competitors.

5. A matter of strategic relevance: European companies need to reassess their risk exposure to economic coercion

As more political clashes can be expected between Europe and China, it will be critical for European companies to assess the likelihood of their business in the country being targeted by economic coercion. They are increasingly pulled between the expectations of the government of their home country and of China. While not seeking to antagonize either, there is room for companies to take principled positions and resist pressure from China. In the changing geopolitical context, companies need to reassess their risk profile in order to evaluate the credibility of potential threats and to navigate business opportunities and political risk.

Some European companies will inevitably be hit by Chinese economic coercion regardless of their best efforts to avoid it. JKT companies provide valuable lessons on how to mitigate the risk and continue to engage in the Chinese market. Regardless of their risk exposure, they have employed diversification strategies to various degrees, either as a precaution or as a reaction to economic coercion. The JKT examples also provide evidence that high market exposure in the form of revenue share and investment footprint in China does not automatically translate to high-risk exposure.

The actual risk exposure is more complex, and each company faces a different level of vulnerability. Taiwanese companies, in particular, are a case in point. Despite being caught up in the political tensions over Taiwan’s sovereignty, their massive business interests in China have rarely been the target of economic coercion. However, increasing political risk is also leading them to diversify more without abandoning the Chinese market.

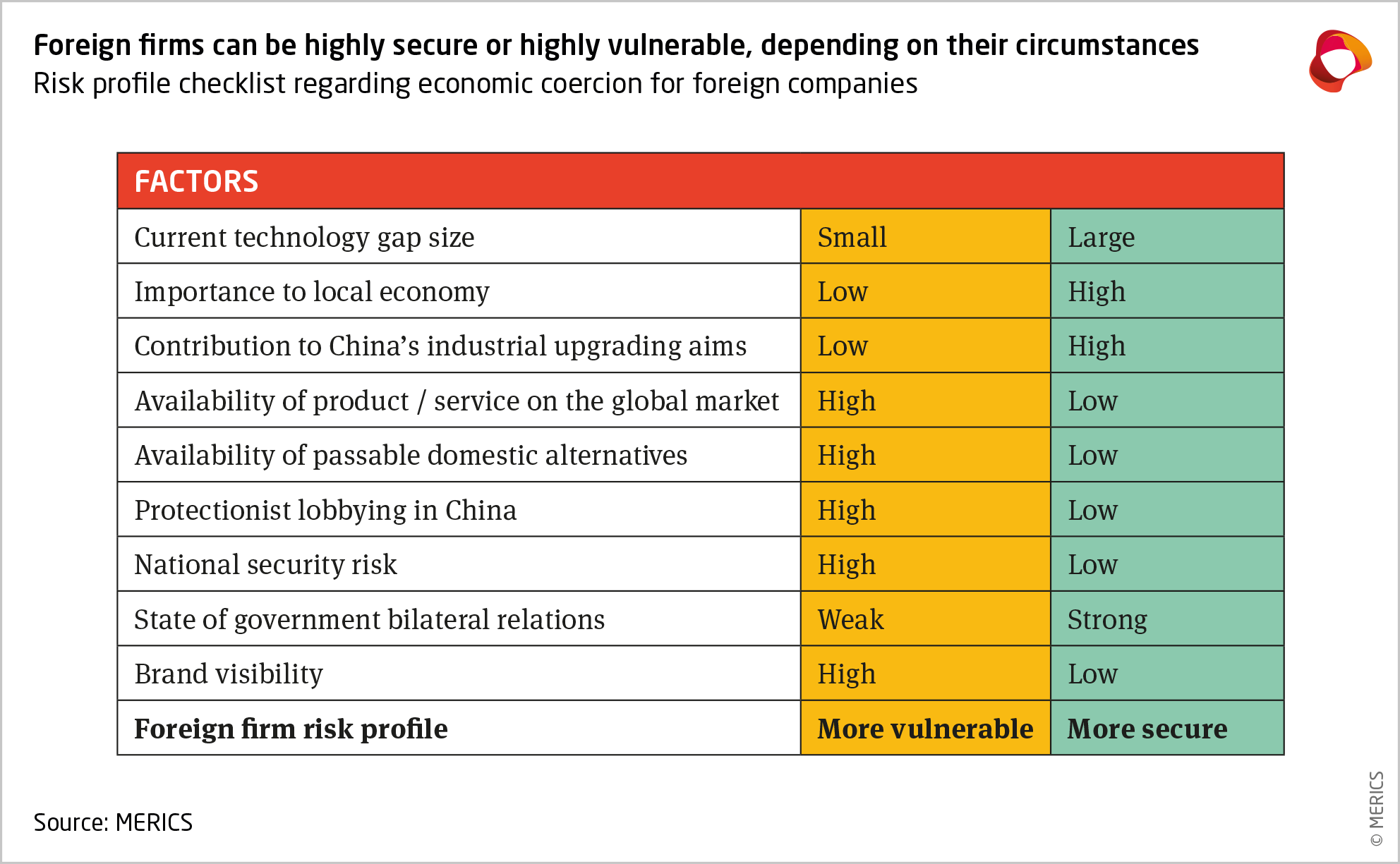

The patterns of China’s past behavior show that numerous factors increase or decrease the likelihood and severity of a company being hit by economic coercion. Primary factors include a company’s level of technology and investment footprint. Foreign firms that produce high-tech or hard-to-replace products are unlikely to be targeted. Those with significant investments in China and that contribute to local employment and taxes are also likely to be in a more secure position.

On the other hand, companies in the commodities, agricultural, consumer goods and services sectors are vulnerable. The extent of their vulnerability is mainly determined by their usefulness for China. For example, Beijing would gladly see the sales of a foreign fashion brand decrease, but it is unlikely to come down hard on a manufacturer of cutting-edge robots or aircraft components. Secondary factors include bilateral government relations and brand visibility.

Exhibit 7

Measuring risk exposure to economic coercion strongly depends on a company’s profile (see Exhibit 7). European companies need to understand their respective role in China’s economy and strategic plans. A realistic assessment of how valuable the company is for the objectives of the local or central government in the country is key.

However, a company’s risk exposure changes over time given the dynamic situation. For example, China is working hard through its industrial policy on closing technological gaps with other countries, which can eventually render European companies irrelevant as technology providers. These companies thus require another safeguard, such as relevance as employers or taxpayers at the local level, or else their vulnerability will increase – especially if they have a high China revenue share.

Highly vulnerable companies will need to be more careful about pursuing market opportunities in China. Their investments could quickly lose value if their business becomes a target of coercion, due to an action of their own or that of others. However, companies that are less vulnerable today must continually reassess their strategic relevance.

China’s responses to infringements on its interests may come across as excessive shows of force, yet in many cases its measures may incur only limited economic costs on their targets. Often it uses economic coercion for signaling and deterrence, going after prominent companies or sectors to deter other companies or governments from crossing certain lines. The obvious choice is to target strategically irrelevant companies (high risk profile). Consumer brands, for example, will be pressured to align themselves prominently with government-approved positions. If they do not, officials may undermine their business operations in China.

Companies with a lower risk profile are far less vulnerable. Even those which derive a large share of their revenue from China can be in a secure position. Were China’s government to target such a company, it would not only put inbound investment and technology at risk, but also potentially lose the benefits of large foreign businesses lobbying their home governments in favor of Chinese interests. Such companies should thus not overestimate their vulnerability – they have far less to fear in speaking out, especially on issues relating to the business environment in China.

As long as European companies and governments are fearful of the potential impact of China’s economic coercion on their operations due to their high market exposure in the country, covert or open threats will be sufficient to water down or even prevent actions that Beijing deems undesirable.

China’s most effective forms of economic coercion are implied pressure and informal measures to disrupt foreign businesses in the country. Fearful of becoming a target, companies might avoid speaking out about the unfair treatment of foreign firms in China or deem it safest to align themselves with the positions and objectives of China’s government. This would be problematic from the perspective of European governments. Having a clearer picture of actual economic vulnerabilities will be a crucial step forward as Europe’s relationship with China becomes more complex.

No comments:

Post a Comment