Gabriel Di Bella, Mark Flanagan, Karim Foda

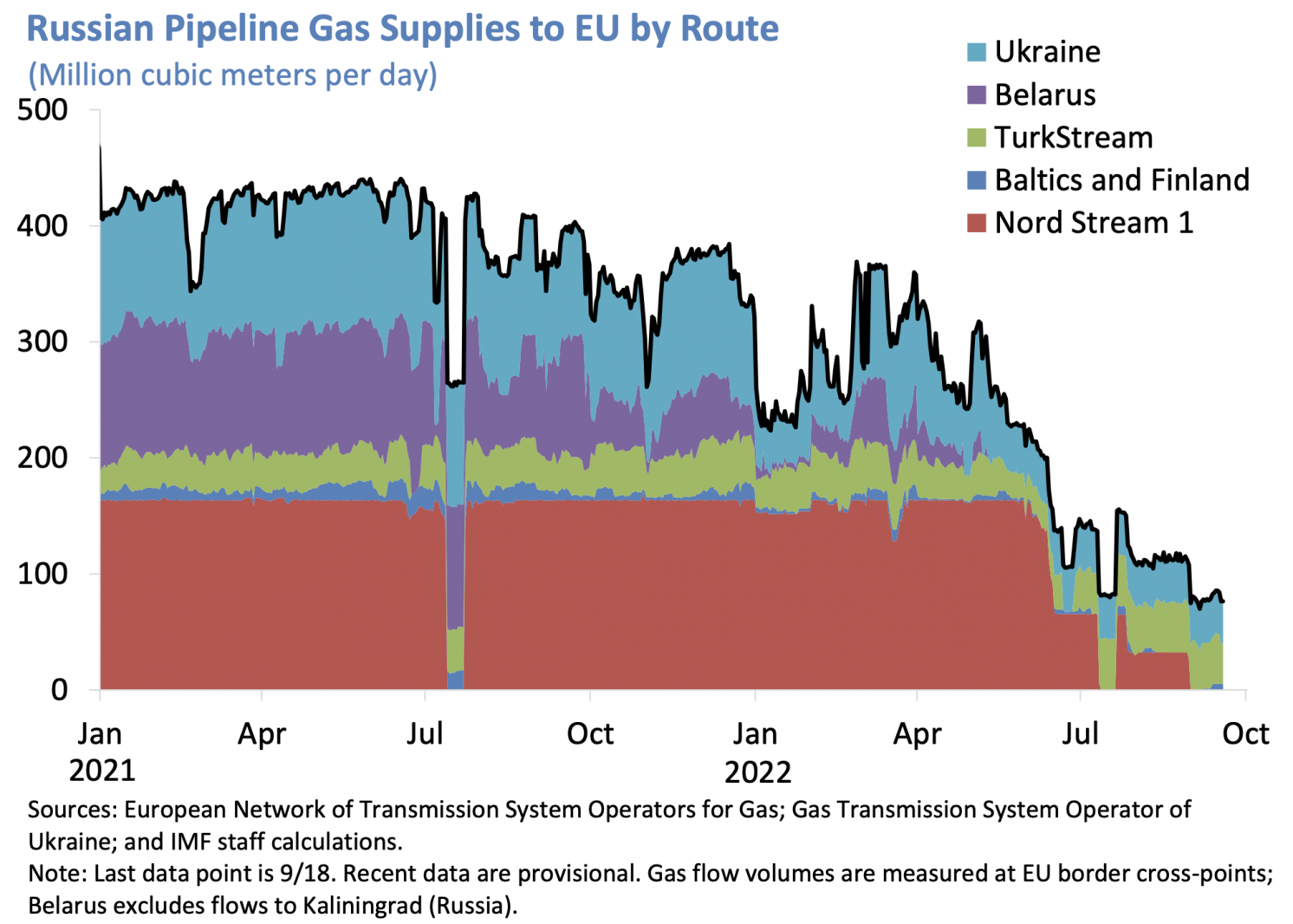

Since the onset of the war in Ukraine, Europe has been in a race to secure new natural gas supplies as it faces a partial shut-off of gas exports from Russia, historically its largest energy supplier. Russian pipeline gas exports have fallen incrementally over the past months and with the indefinite suspension of Russian gas flows through Nord Stream I. As of September, Russian flows now stand at 15% of 2019 average levels (Figure 1). This has led to sky-rocketing European wholesale natural gas prices which peaked at over ten times their historical average in August 2022.

Figure 1 Russian pipeline gas supplies to EU by route

(Million cubic metres per day)

Given the unique nature of the natural gas market – which is less integrated at a global scale than most other commodity markets, thus making substitution more difficult for both producer and consumer countries – a large literature has been debating how Europe can and should adjust its natural gas policy, what it implies for global energy markets, and what the effects of reduced Russian flows are for Europe (Martin and Weder di Mauro 2022, Arezki and Paduano 2022, Feliciano et al. 2022). Highlighting the unprecedented nature of the shock, estimates for the economic impact of a full suspension of Russian gas deliveries produced in the months after the outbreak of the war varied widely. In the case of Germany, for example, from below 1% (Bachmann et al. 2022) to a deep economic contraction (Krebs 2022),

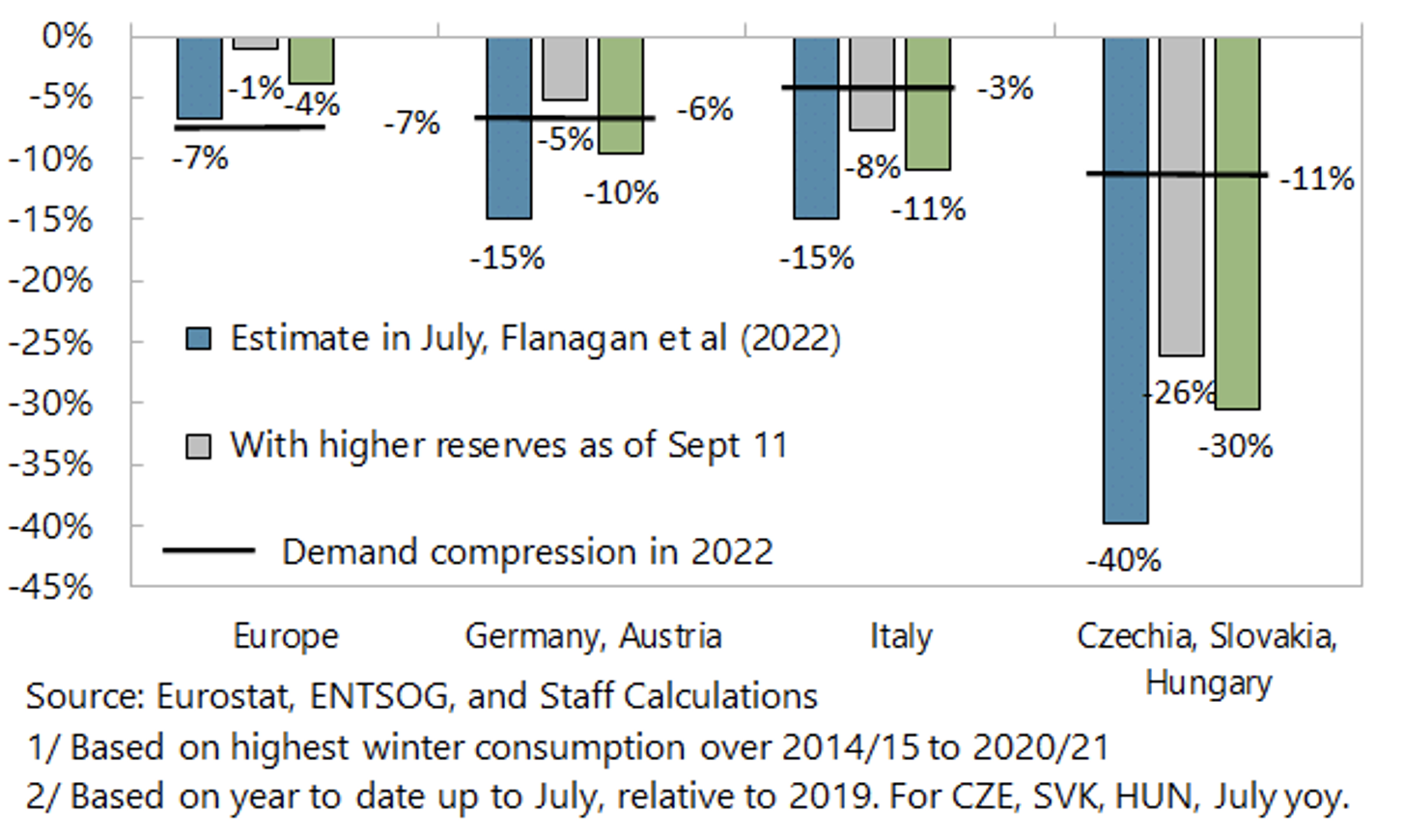

In July, when Russian gas flows had fallen to one-quarter of 2019 levels and European storage levels stood below their historical averages, we highlighted that the impact of a full Russian gas shutoff would be highly heterogenous across Europe. In addition, we argued that the severity of the GDP impact would depend importantly on three key aspects: (i) the availability of alternatives supplies, (ii) the degree of fragmentation in gas markets, which would limit the ability of the global liquefied natural gas (LNG) market to buffer the shock, and (iii) the degree of endogenous gas demand adjustment that would be achieve through higher retail prices (Flanagan et al. 2022). 1 We concluded that in some of the most-affected countries in Central and Eastern Europe—Hungary, the Slovak Republic, and the Czech Republic—there was a risk of shortages of as much as 40% of gas consumption and of gross domestic product shrinking by up to 6% relative to the counterfactual over a 12 month window. The impacts, however, could be mitigated by securing alternative supplies and energy sources, easing infrastructure bottlenecks, encouraging energy savings while protecting vulnerable households, and expanding solidarity agreements to share gas across countries.

Now that we are getting closer to the winter and Russian gas flows have been further curtailed, it is worth taking another look at where Europe stands. For Europe as a whole, higher non-Russian supplies over the summer provided a window to refill storage levels to normal seasonal levels. This, and some economically costly reduction in gas consumption, implies that the risk of widespread shortages over the winter have been significantly reduced. However, two important caveats apply to this conclusion. First, a cold winter (in Europe or Asia) could still make for an extremely tight demand/supply balance – not only in the winter itself but in the following months as reserves need to be rebuilt. And second, supply shortfalls in the most exposed countries, where endogenous demand adjustment remains far from what would be required in a full shutoff scenario over a 12-month horizon, remain a real risk (Figure 2).

Figure 2 Gas shortfall over the next 12 months under a full shut-off of Russian gas

(Percent of annual consumption)

Evolving vulnerability: Developments with pipes, ports, and liquefied natural gas trade

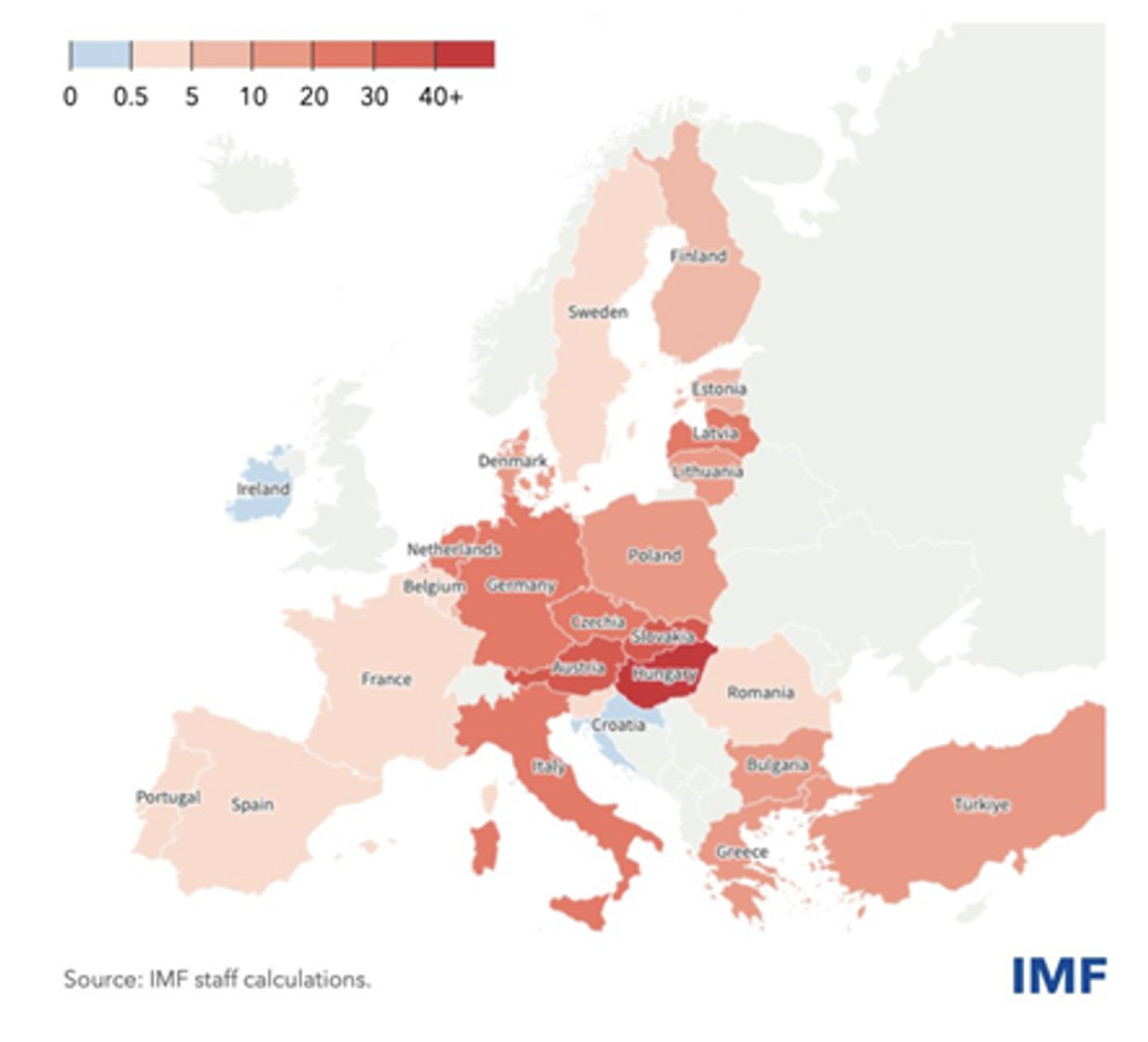

Dependence on Russia for gas and other energy sources varies widely by nation (Figure 3). As of 2020, some economies strongly relied on Russian gas imports for their energy needs, especially the Czech Republic and Hungary.

Figure 3 Russian gas dependence

(Russian gas as a share of total energy consumption, 2020, percent)

The major gas arteries from Russia enter through Germany, Poland, Ukraine, and Turkey, accounting for 42% of gas import capacity. Other pipelines from Norway, the UK, Northern Africa, and the Caspian region account for 30%. Liquefied natural gas (LNG), most of which arrives by ship, accounts for the remainder of import capacity, with the largest share arriving at terminals in Spain, France, and Italy.

However, technical constraints in transmission within Europe create potential bottlenecks that could fragment the European gas market. Spain, for example, is the EU’s largest LNG importer, with more than a third of total EU capacity, but it can send only a tenth of what it imports to neighbouring France. Constraints exist within France, Italy, and Germany. And pipelines designed to flow east to west could leave other countries, especially in Central Europe, effectively disconnected from Europe’s spare capacity.

Over the past months there has been important progress, however. The Baltic pipeline has been an important addition of infrastructure allowing greater supplies from Norway to Poland and Central and Eastern Europe. Germany has rented four floating LNG terminals and the first one is expected to be onstream by the end of the year, providing much needed additional capacity to import greater volumes into Northern Germany. In addition, France has said that natural gas exports to Germany will begin in October. Further important infrastructure could be built, including pipeline capacity across the Pyrenees to fully connect Iberian LNG capacity to the rest of Europe.

Gas consumption: Encouraging early signs of adjustment

The EU has agreed a voluntary natural gas consumption reduction target of 15% this winter. Evidence for Germany suggests that demand adjustment is indeed taking place, with Germany on target to meet this goal (Chen and Sher 2022). Looking more broadly at European countries shows an average reduction in gas consumption of 6% year-to-date. Analysis by McWilliams et al. (2022) suggests that the price effect is playing an important role in achieving these reductions in demand, with a strong correlation between increases in end-user gas prices and reductions in demand. While these demand reductions are a prerequisite to managing the transition away from Russian gas, it is important to note that since much of the adjustment is driven by industry there will be a negative impact on output.

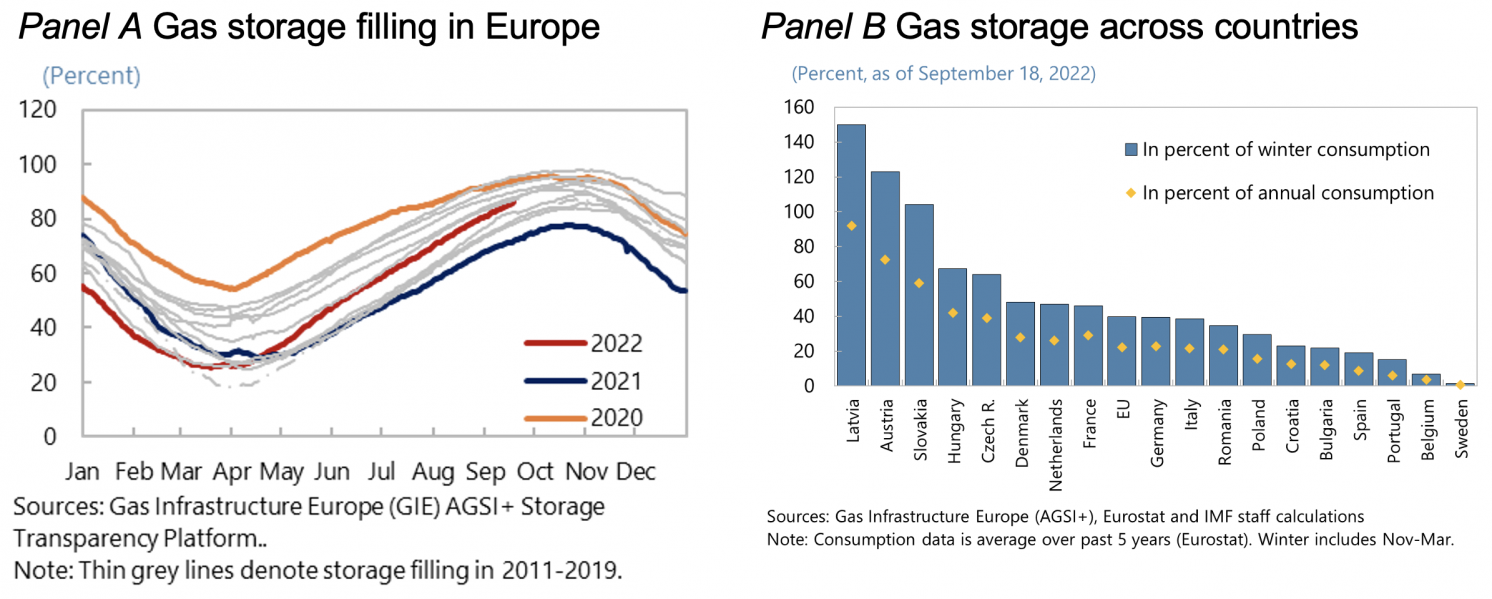

Gas storage: Hitting targets

Europe came into Spring 2022 with storage levels severely depleted, raising the risk of entering the following winter with insufficient reserves, especially with Russian flows already reduced. However, higher LNG imports and greater non-Russian pipeline flows (mainly from Norway and partly Algeria) have managed to keep overall gas imports to Europe largely unchanged. The extremely high wholesale gas price in Europe has been key in attracting these alternative flows (especially LNG).

These imports, coupled with reduced gas consumption, have allowed storage levels to increase above average seasonal levels (Figure 4, Panel A). Indeed, Europe has achieved its objective of increasing reserves to 80% of capacity two months ahead of schedule (1 November). And while in some countries like the UK reserve capacity is a very low share of annual consumption, in many of the most vulnerable countries in Central and Eastern Europe, reserves cover a large share of annual consumption. As of mid-September, EU gas storage was around 86% of capacity, corresponding to around 40% of winter consumption (Figure 4, Panel B).

Figure 4 Gas storage

The situation to date and the road ahead

To date, European infrastructure and global supply have been able to cope with the drop in Russian gas deliveries. This is in line with our earlier assessment that a reduction of around 70% of Russian gas could be managed by accessing alternative sources. Coupled with the reduction in demand observed to date and the much-improved gas storage situation, Europe now finds itself better prepared for the winter. The focus has for now shifted more towards the impact of extremely high prices which are fuelling inflation and hampering growth, rather than outright shortages. The two concerns are intimately linked, however, given the role of high prices in attracting alternative supplies and reducing demand. And in a generalised shut-off, diversification would be more difficult, with the possibility of re-routing gas within Europe reduced (as bottlenecks could show up) and substituting gas for alternative fuels made more difficult by even higher demand for these. Europe continues to be at risk of shortages, especially during a cold winter.

Europe should continue to focus on developing alternative energy sources, completing critical natural gas infrastructure projects which would help avoid internal bottlenecks, and reducing demand in a growth-friendly manner. The focus should be not only on the coming winter but also on the next: replenishing storage for the 2023/24 winter will be harder if Russian gas flows cease completely. Bottlenecks in the LNG export infrastructure in the US, Australia, and elsewhere, which are used at capacity, need also to be addressed to further substitute Russian pipeline gas by liquified natural gas and to build a more integrated global gas market.

No comments:

Post a Comment