Homi Kharas and Charlotte Rivard

Strong headwinds suggest that 2023 will be a difficult year for global economic development. Avoiding setbacks will be at least as important as making renewed progress. Developing countries will continue to face overlapping crises with little to no fiscal space for addressing them. In the short term, debt and humanitarian distress are pressing threats, while in the longer term, climate action and spending on sustainable development goals (SDGs) remain priorities. If ignored, any one of these areas could have serious consequences for millions of people. If a critical mass of countries were to be adversely affected, it could create systemic failure in the global capacity to provide safety nets for people and resilience for economies.

Plans to avoid the worst outcomes will require some common features. At the country level, there need to be better policies, stronger institutions, and sound economic governance. At the international level, there need to be larger flows of official finance.

It will not be feasible to protect all countries from all types of risk. The human and financial resources to respond to crises are limited. The global community—major international organizations and large donors—needs a plan to avoid systemic risk and a watchlist of systemically important countries. Such a plan must triage and focus on those countries where the number of affected people is the largest. This does not imply that small countries should be ignored, simply that they have smaller spillover consequences for the rest of the world, and from a financial viewpoint, their issues are more manageable, so they can be dealt with as and when the need arises.

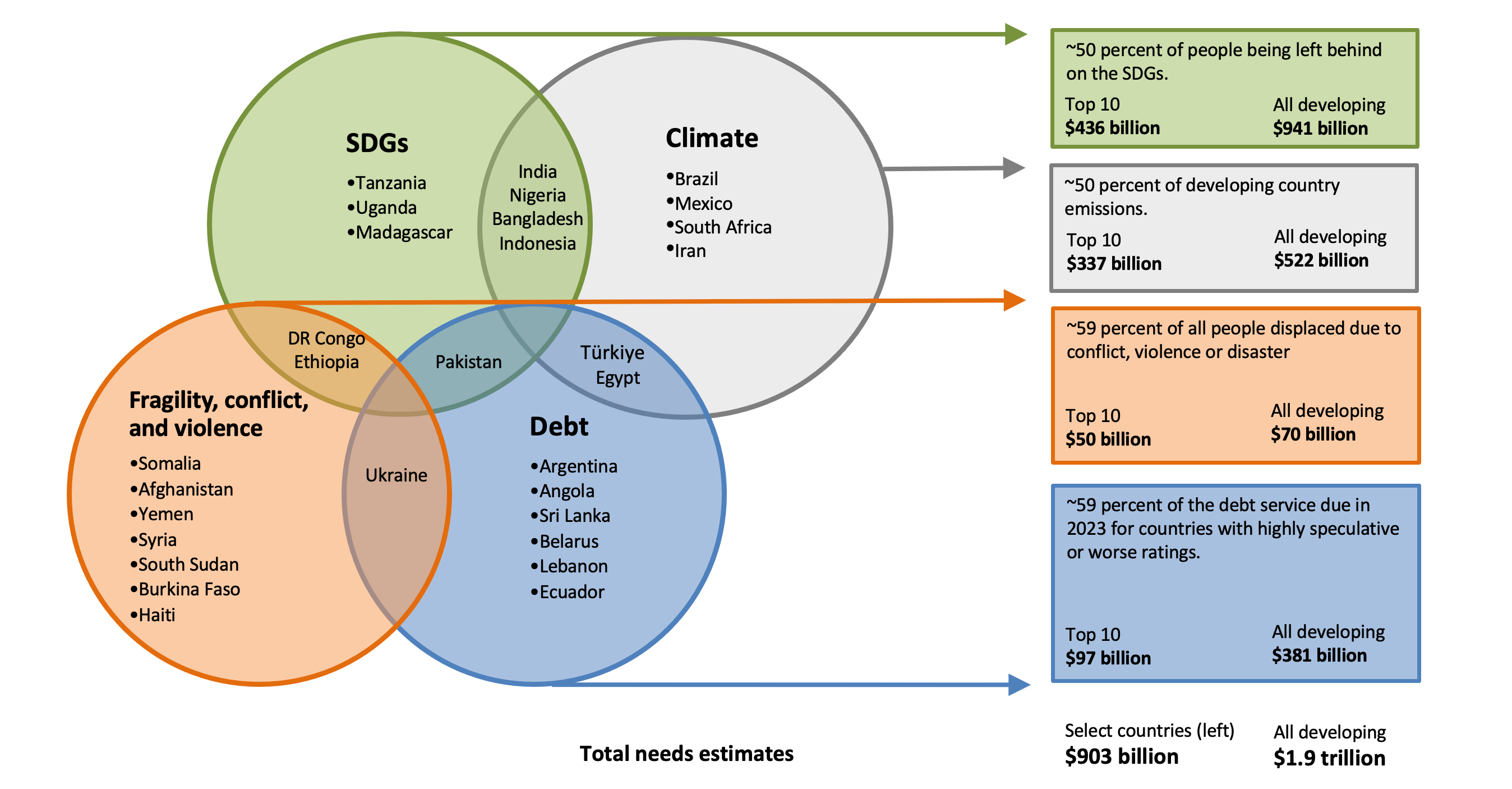

Which countries should be on a watchlist of those who could trigger a systemic failure, and what are the resource gaps involved? We consider below four priority areas in economic development where there are major gaps: (1) SDGs, (2) climate, (3) debt vulnerability, and (4) fragility, conflict, and violence.

SDGs

This year marks the mid-point of the SDG time horizon (2015-2030). Heads of state will gather in September at the United Nations to take stock of progress. They will find that all the SDG targets for 2030 are off track and some indicators are even going backward. Early findings from forthcoming work (see sources under Figure 1) suggest that 10 countries account for roughly half the number of people left behind on a cross-section of key SDG targets. For example, there are about 600 million people still living in extreme poverty and millions more without adequate food, education, healthcare, or access to modern energy. Previous work on “building the SDG economy” estimated that roughly $1 trillion in additional spending is needed for developing countries to achieve the sustainable development goals. The 10 countries with the most “people being left behind” account for about half the financial gap. Without tangible progress on SDG financing this year, or at least a plan for an acceleration, there is a risk of a “lost generation.” Confidence in global programs and solutions will also inevitably fall further.

Climate

Developing countries (excluding China) comprise 38 percent of current global greenhouse gas emissions and are expected to emit about half of annual emissions by 2030. While a “green transition” is underway in many developing countries, it is limited by inadequate financing. Less than 20 percent of installed global solar capacity is in developing countries (excluding China), even though these countries have some of the most favorable climatic conditions in the world. The reason is simple: the higher cost of financing in developing countries. An estimated $500 billion is needed this year, in addition to current funds, to finance climate mitigation and adaptation efforts in developing countries—sustainable infrastructure projects and natural climate solutions in agriculture, forestry, and land use. (Note this is far more than the oft-referenced $100 billion of climate finance promised by developed countries, a pledge that has still not been met.) Further, with the collapse of private financing in 2022, many sustainable infrastructure projects have been put on the back burner. The 10 countries with the largest climate financing gaps need around two-thirds of the total climate financing gap, or $350 billion. These 10 countries emit roughly half of developing country emissions (excluding China). If they do not act more aggressively on climate, prospects for keeping temperature increases below 1.5 degrees, or even 2 degrees, will dim.

Debt

In 2023, developing countries owe an estimated $381 billion in debt service on medium- and long-term external debt according to the World Bank International Debt Statistics. 53 countries have credit rating classifications estimated to be “highly speculative” or worse. This subset of developing countries owes $166 billion in debt service in 2023. The top 10 debtors alone owe almost 60 percent of this debt service, or a quarter of total debt service due by developing countries. The current debt resolution system would struggle to handle more countries. Only three countries are currently renegotiating their debt under the G-20-led Common Framework, and most large debtors are ineligible to participate. The inefficiency of approaching the issue on a case-by-case basis raises the likelihood that more developing countries will lose their hard-earned access to private capital markets and that 2023 will see a return to systemic debt crises.

While the war in Ukraine consistently occupied the headlines in 2022, many other countries faced urgent humanitarian concerns—from natural disasters, to armed conflict, food crises, and political instability. The IRC publishes an Emergency Watchlist of 10 countries most at risk of a humanitarian crisis. The latest watchlist countries accounted for nearly 60 percent of people displaced due to conflict, violence, or disaster across all countries in 2021. In the most recent past, only about 50 percent of the humanitarian appeals for these countries (excluding Ukraine) was met according to the U.N. Office for the Coordination of Humanitarian Affairs (OCHA). They only received $17 billion in 2021 according to OECD statistics but had costs and losses estimated at $32 billion. In addition, the Kiel Institute for the World Economy estimates that Ukraine received $17.8 billion in humanitarian aid between January 24 to November 20, 2022. If these 10 countries have the same order of magnitude of losses in 2023 as they did in 2021, costs and losses will amount to $50 billion.

KEY TAKEAWAYS

Figure 1 below provides an overview of the top 10 countries in each risk category. In all, there are 30 different countries that need to be watched (ten countries are on two lists). The aggregate resource gap in those countries amounts to $903 billion in 2023. Most of this will need to come from domestic sources, but a substantial amount will surely be needed in external assistance. Donors and official financing agencies should make contingency plans. (The World Bank already announced a “surge” financing program that will last through June.)

The financing needs are not simply concentrated in a handful of countries that have multiple overlapping crises. Rather, quite different sets of countries are affected by each vulnerability, resulting in many different countries requiring funds. The current system is not fit for this scale of financing needs or concurrent crises.

There are early-stage discussions on what to do next. Discussions at the G-20 and other forums on expanding the multilateral development banks are ongoing. Some funds, notably the Green Climate Fund is up for replenishment this year. But there is little indication that rich country governments are willing to support a huge step-up in official finance. There need to be new and innovative mechanisms for channeling resources to developing countries. Ideas abound: new issuance of special drawing rights (SDRs), credits for carbon offset sales in voluntary carbon markets, ecoservice payments, taxes on fossil fuels, state-contingent clauses in financial instruments. These ideas are still at a formative stage. It is time for more brainstorming in 2023 to see where the possibilities lie, else global development will continue to lurch from crisis to crisis.

Figure 1: Estimated developing country vulnerabilities and financing needs for 2023

Note: Excludes Russia and China from analysis. The ordering of countries is by SDG performance, climate financing gaps, debt service payments, and emergency watch list countries according to the order by IRC (with the exception of countries in the overlaps).

Sources: International Rescue Committee; OECD Statistics; and Internal Displacement Monitoring Centre for fragility, violence, and conflict; EDGAR; World Emissions Clock; and Bhattacharya et al (2021) for climate; International Debt Statistics for debt; and preliminary results from Kharas, McArthur, and Onyechi (forthcoming) for SDGs.

No comments:

Post a Comment