By Severin Fischer

In this article, Severin Fischer discusses three of the most important recent and upcoming technological advancements in energy – horizontal drilling with hydraulic fracturing, photovoltaics and batteries – and their potential impact on international politics. Further, he outlines why China and the US will have the biggest impact on future discussions on the geopolitics of energy. Technological change has a tremendous impact on societies in general, including international politics. This chapter discusses the most important recent and upcoming technological advancements in energy – horizontal drilling with hydraulic fracturing, photovoltaics, and batteries – and their possible influence on geopolitical dynamics. For different reasons, China and the US will have the biggest impact on the way we will discuss the geopolitics of energy in the future.

In this article, Severin Fischer discusses three of the most important recent and upcoming technological advancements in energy – horizontal drilling with hydraulic fracturing, photovoltaics and batteries – and their potential impact on international politics. Further, he outlines why China and the US will have the biggest impact on future discussions on the geopolitics of energy. Technological change has a tremendous impact on societies in general, including international politics. This chapter discusses the most important recent and upcoming technological advancements in energy – horizontal drilling with hydraulic fracturing, photovoltaics, and batteries – and their possible influence on geopolitical dynamics. For different reasons, China and the US will have the biggest impact on the way we will discuss the geopolitics of energy in the future.

The public pressure caused by livestream pictures from Tahrir Square during the Arab Spring, the propaganda machinery of the so-called “Islamic State”, and US President Donald J. Trump’s public communication on foreign policy via social media have one thing in common: All three examples show that technological change and international politics are closely linked. While new communication technologies are certainly among the more obvious examples for the fundamental impact of rapid technological change, other sectors are also seeing shifts of similar magnitude.

In the energy sector, technological progress used to unfold over decades rather than months. In some cases, change was accelerated by political decisions. When Winston Churchill, as First Lord of the British Admiralty, urged his government to use oil instead of domestic coal to fuel the Royal Navy in the run-up to World War I, this not only impacted the outcome of the war and therefore the course of history, but also revolutionized maritime transport in the years to come.1 In other cases, exploration and technological progress in drilling techniques turned the Middle East, which had been a relatively poor region during the early 20th century, into a geopolitical hotspot in the 1960s and 1970s. Technological innovations, though enthusiastically embraced, did not always become the global success stories their proponents had anticipated. This is true for nuclear energy, a technology that was celebrated as a source of cheap and clean electricity for everyone, but has not lived up to projections.

Employees row a boat as they examine solar panel boards at a pond in Lianyungang, Jiangsu Province, China. China Stringer Network / Reuters

Changes in the energy sector may have an impact on various dimensions of international politics, such as security, trade, or environmental policies. However, it is difficult to project their range and impact beforehand. In this sense, this study is exploratory and describes trends in technological developments in the energy sector by examining three technological developments at different stages of readiness and deployment. The first is a set of technologies that can be summarized under the title “hydraulic fracturing”, which has influenced the position of the US in global energy markets and will do so in the coming years. The second technology trend is the use of solar energy from photovoltaic cells, also commonly referred to as “solar panels”. With rapidly decreasing costs and a massive extension of industrial production, solar energy is in the process of revolutionizing energy systems around the globe. The third part concentrates on the effects of the upcoming wide-scale distribution of batteries, not only for the use of electric vehicles, but also for application in microgrids and for other uses. These three technologies have been chosen for analysis based on the remarkable gains in economic efficiency and productivity that they offer, their potential for bringing structural change to the energy sector, and various specific endogenic dynamics such as cross-cutting effects or market design features, e.g., the possibility to apply solar arrays and batteries on individual small-scale level. Analyzing three technological developments does not provide an exhaustive picture, of course. But they offer the biggest potential for disruption due to the way they are changing the mode of thinking about energy. All three technological developments are already influencing the role of energy in international politics today, or will do so in the future, and should therefore be watched closely.

The Fracking Revolution: The Emergence of US “Energy Dominance”

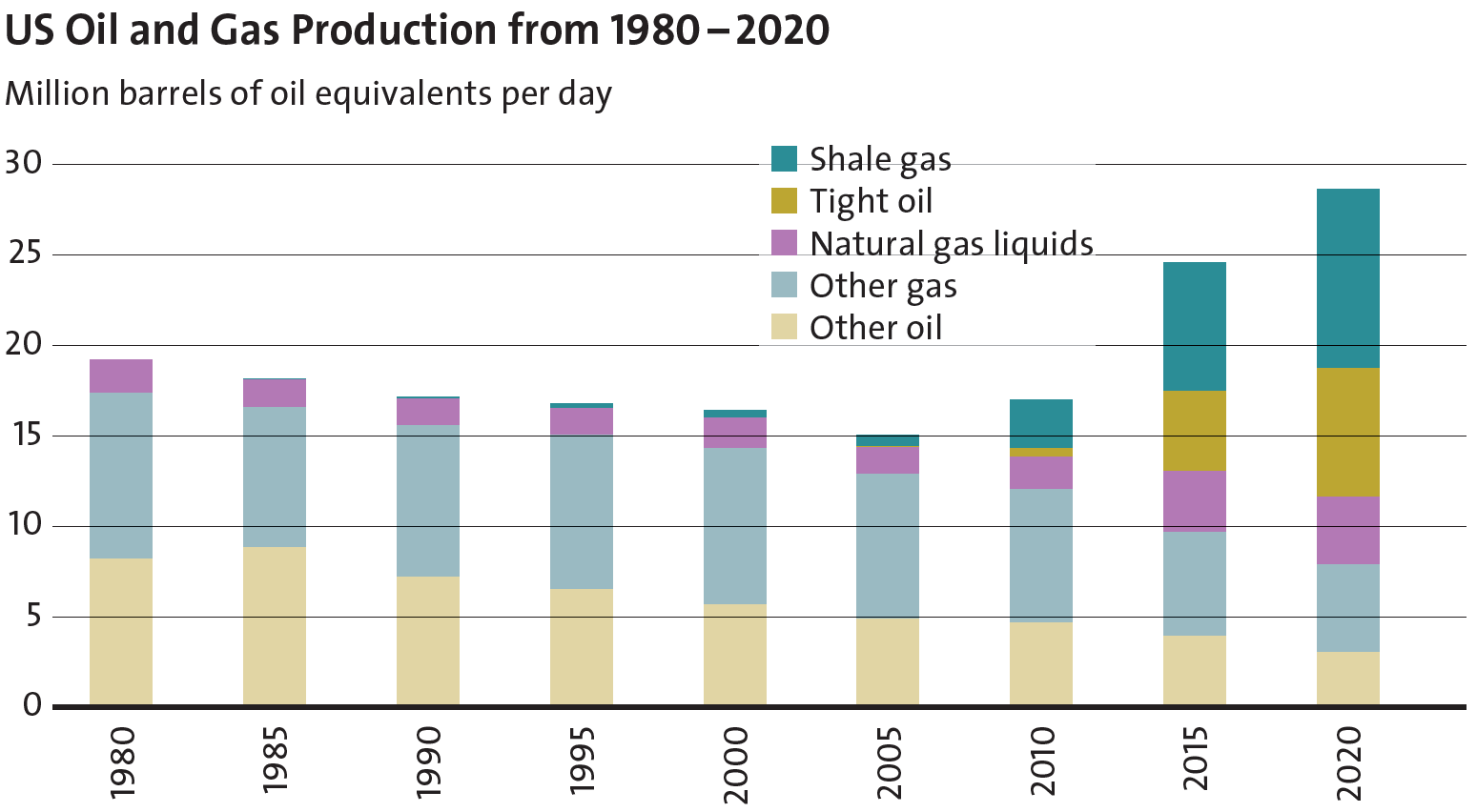

Hydraulic fracturing (“fracking”) in oil and gas extraction is not a specifically new technology in itself, but did not prove cost-efficient when the first trials were made in the early 1950s. During the first years of the 2000s, oil and gas firms in the US started to experiment with the combination of hydraulic fracturing – the use of high pressure and fracturing stimulation– and horizontal drilling, in order to access oil and gas reserves in shale and other formations. By pressing water, sand, and other materials into promising geological layers and rocks, small fractures emerge through which oil and gas are released and can be pumped to the surface. Initially, the technology was only used to “stimulate” existing reservoirs. Only recently have companies tried to access completely new formations by using this technology, with the resulting products now commonly referred to as “shale gas” and “tight oil”.

Initially, fracking was largely neglected by the big international oil and gas companies. Then, some independent firms experimenting in the Texan Barnett field were successful in reducing costs and made shale gas economically viable. Today’s major shale gas fields (Marcellus, Eagle Ford, and Hayneville) have been developed since 2008. With know-how gained from the experiences with shale gas production, the extraction of tight oil started to kick off around 2011 in the Permian Basin and the Bakken field. By 2016, the total US production of natural gas was approximately one-third higher than in 2005, while half of today’s production stems from shale formations, or is a by-product of tight oil extraction. By late 2017, US oil production had doubled compared to 2008, hitting the 1970s maximum production level of just above 10 million barrels per day, half of which is supplied by tight oil. The US is set to surpass Saudi Arabia’s production levels in 2018, closing the gap to the world’s number one oil producer, Russia.

The important change that hydraulic fracturing brought to the market not only consists in the additional quantities available, but also concerns the structure and dynamic of this new oil and gas business segment. While large corporations are used to planning long-term investments in conventional fields onshore and offshore, including decade-long preparation and operation, shale gas and tight oil extraction has proven to be a very flexible and mobile business oriented toward short-term gains. Typically, tight oil wells decline by about 60 per cent in the first year, followed by another 25 per cent in the second year.2 Consequently, the fracking industry is under constant pressure to discover and drill new wells on a yearly basis. At the same time, the operational efficiency of individual wells has been improved tremendously during the last couple of years. While the industry’s main focus in the first years was on developing new wells, more recently, the productivity of the individual wells has gained more attention. In the Bakken field, the productivity of an individual rig increased by a factor of six between 2011 and 2016.3 Rig productivity was also the key factor that helped the industry to survive the oil price crash of the years 2014 – 2016.

One interesting aspect concerning the development of hydraulic fracturing is the remarkable fact that deployment of these technologies has so far been limited geographically to North America. Certainly, the geological conditions in the different oil- and gas-producing regions of the US are favorable. However, they are clearly not unique. In certain regions of China, Europe, North Africa, or South America, shale formations look promising as well. There are three primary reasons for the reluctance to move into fracking in other parts of the world: First, the regulatory framework is an essential factor. While in the US, private landowners had an economic interest in allowing the extraction of resources, taxation and environmental regulation have slowed the deployment of these technologies in Europe. Second, the current low price environment for oil and gas has limited the willingness to invest in unknown territories with uncertain results. Third, and most importantly, one main reason for the concentration of fracking companies in the US is the availability of various services and materials related to The industry. The whole value chain around the industry is a crucial factor, ranging from geological exploration and the availability of fracking material to the ability to transport oil and gas to market. Of course, none of these factors precludes a future extension of fracking beyond the US. It just hasn‘t happened yet on a relevant scale. Should fracking technologies be used in other places around the globe as well and bring revenue streams to governments, the age of abundance for hydrocarbons could last much longer than most people think.

Looking at the effects of extended oil and gas production in the US, it is notable that the dynamics of the two commodity markets are quite different. In the traditionally rather regionally-oriented gas markets, studies expected the US to become a significant importer of Liquefied Natural Gas (LNG) from the year 2010 onwards. This projection had to be reversed fundamentally with the US fracking boom, which made additional volumes of LNG available for other consumers, caused oil and gas prices to become de-linked, and led to a price drop that affected gas markets on a global scale. With the installation of export LNG terminals in the US, even more gas will be available in the years to come. Asian consumers in particular are already betting on the import of relatively cheap LNG cargos, which would allow them to satisfy a growing energy demand with less polluting fuels.

While LNG was a niche market in the past and has only recently started to grow, oil has been a global commodity for many decades. With the growth of tight oil production in the US in the range of some 5 per cent of global oil output, supply has outpaced demand by far, resulting in a remarkable fall of prices from over 100 USD to 30 USD per barrel within just two years between 2014 and 2016. While OPEC, the major group of oil exporters, initially decided to leave its own output untouched, hoping to squeeze out the new competitors from the US, it changed course at the end of 2016. Together with Russia and other oil exporters, OPEC agreed on a production cut in order to rebalance supply and demand. After the so-called “OPEC+” deal proved stable for more than one year, oil prices have come back to a level of around 70 USD per barrel.4 Although tight-oil producers in the US were troubled and saw some economic hardship, the abovementioned productivity gains kept them in the market. In the future, the global oil market will continue to be affected by this new group of suppliers, who are relatively free from political influence and highly flexible. This structural difference compared to the state-controlled oil and gas companies of Saudi Arabia or Russia and to the traditional Western companies with their long-term projects and investment plans will fundamentally change the dynamics of hydrocarbon markets.

Looking at the level of politics and especially the international arena, the oil and gas boom has first and foremost influenced the self-perception of the US. The oil crises of the 1970s and 1980s had a long-term effect on the role of energy in the analysis of security threats and the foreign policy domain of the country. The struggle for “energy independence” seemed to have been lost in the early 2000s, when projections showed energy imports from foreign sources apparently predestined to go up. A constant dialog with Saudi Arabia on market liquidity, the demand for open markets in general, the protection of maritime shipping lanes, and safeguards through the International Energy Agency’s (IEA) inventory system were central instruments for dealing with threats to energy security. While the administration of Barack Obama already witnessed and domestically supported the turnaround in the energy landscape initiated by the fracking industry, the change in rhetoric has only happened recently under President Donald J. Trump and his energy secretary, Rick Perry. What used to be the desire to become “energy independent” has shifted to the new paradigm of “energy dominance”. During the course of 2017, the administration elaborated on the meaning of this proposition: While two aspects of the concept – the creation of jobs for US workers in the field of energy and the availability of cheap energy for US families – might be of lesser significance for international relations, the aim “to be no longer vulnerable to foreign regimes that use energy as an economic weapon” could lead to different conclusions.5

Based on this proposition, one critical conclusion might be that the administration will ask itself sooner or later why US taxpayers should invest in the functioning of the global oil trade by guaranteeing the safe passage of maritime transports. As in the context of NATO, President Trump might be tempted to ask allies to contribute their fair share to the military protection of transport routes for global oil trade. As has become obvious in the recent Saudi-Qatari dispute, the US government’s willingness and capacity to solve crises with an energy dimension seem to be less developed than would have been the case some years ago.

Another worrisome effect of the new strategy could be the use of energy as an instrument of US foreign policy. Urging allies to buy US LNG in order to diversify away from other suppliers (and reduce the nation’s trade deficit) runs contrary to the plea for open markets repeatedly heard from US administrations over the past decades. The vocal concerns about Europe’s energy security, which were referenced in the case of the new unilateral sanctions regime against Russia, now dovetail with the economic interests of the US fracking industry. If Washington is willing to use energy as a means of foreign policy, it will be difficult to explain to others why this would be the wrong approach to global cooperation.6 Nevertheless, it will be difficult for the administration to force private actors such as LNG suppliers or tight oil producers to follow state orders about where to export their products. If Asian buyers are willing to pay a higher price than their European counterparts, LNG will be delivered to Asia, not to Europe.

While the US foreign policy strategy on energy is still in the process of development, the effects on other suppliers and their behavior are already visible. For OPEC as well as for Russia, the drop in prices and the availability of additional supplies on world markets constitutes first and foremost a price problem, and consequently a revenue problem. The production cuts and the low price environment threaten state budgets and necessitate domestic spending cuts. At the same time, they also make reforms and the development of new business models, as in the case of Saudi Arabia’s transformative “Vision 2030”, more difficult. Since the US role as the world’s biggest hydrocarbon producer is expected to evolve over the coming years, the world will have to get used to this new unexpected situation, which was brought about by the experiments of a few small drilling firms in the Midwest.

The Solar Revolution: It Has Only Started

As in the case of hydraulic fracturing, the use of solar energy, specifically photovoltaics (PV), is not a recent invention, but has been around for decades. There were even solar panels installed on the roof of the White House during the late 1970s. The energy crisis of the 1970s forced governments to consider alternatives to oil, one being solar energy. Although many early attempts can be noted, the economics and the lack of political support prevented solar energy from playing a role in the world’s energy system. In fact, it was research and development in Japan as well as the decision of the German federal parliament to support renewable energies with a feed-in tariff from the year 2000 onwards that helped the small niche of PV producers to grow in size, prove their viability, and make impressive progress on economic efficiency. Germany, later joined by some North American and European states, invested billions of euros of public or electricity consumers’ money into the large-scale demonstration of the viability of exploiting solar energy, both on private houses and as large-scale power plants in the countryside. However, without public support via feed-in tariffs and other mechanisms to enable investments, PV electricity production was not able to compete on electricity markets. This situation has changed.

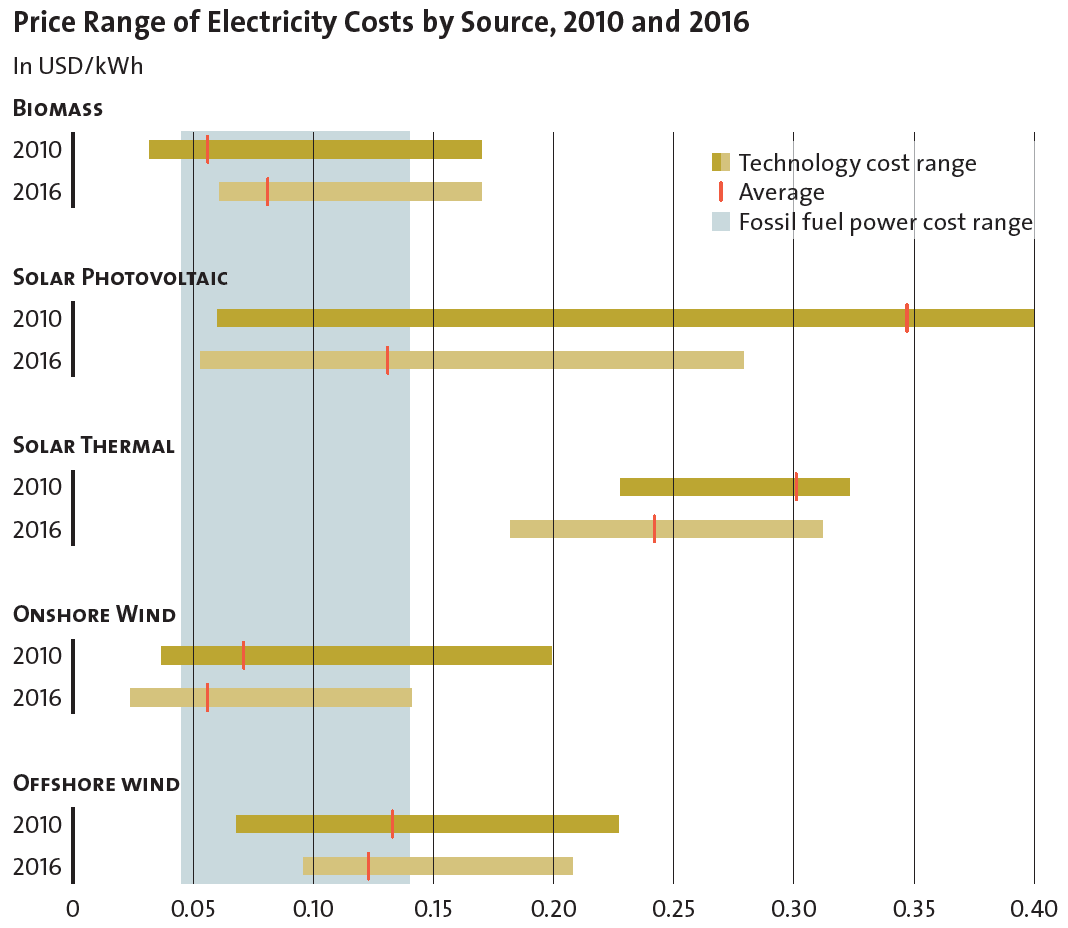

The year 2016 marked an important waypoint for solar energy. As the International Energy Agency (IEA) confirmed in a report, with more than 74 GW in 2016 alone, PV constituted the largest part of all additional electricity generation, easily surpassing coal, wind, and natural gas.7 At the same time, prices in recent auctions dropped to less than 0.05 USD per kWh in some world regions, and levelized costs can now compete with those of electricity generated by burning fossil fuels. Even under conservative estimates, solar power will be the largest renewable energy growth factor over the coming years in a world that is in fact betting more and more on clean energy. In an optimistic scenario, PV will even contribute an additional 1,150 GW by 2022 globally, which would equal nearly six times the already installed electricity generation capacity of Germany in 2016 – from all energy sources.

Source: International Renewable Energy Agency (IRENA), “Levelised Cost of Electricity 2010 – 2016”, resourceirena.irena.org/gateway (2017).

Installed capacity is not the same as generated electricity, of course. Compared to fossil or nuclear power plants, solar power plants have less operating time and feature greater discrepancies between capacity and actual electricity generation. Therefore, the share of solar as a part of global electricity consumption will not increase as quickly as the installed capacity. Nevertheless, as a new player in electricity production, solar energy will significantly change the overall structural picture in many countries. Especially in certain regions of the developing world that previously had no electricity supply at all, temporary access to electricity will be a vast improvement over the present situation of having no access to electricity at all.

While the development of solar energy effectively started in Europe and the US, China is the biggest player on the market today. About half of all new solar power plants installed in 2016 were in China. At the same time, 60 per cent of global solar manufacturing capacity is located in China, up from just 4 per cent in 2009.8 This development was no accident. The Chinese government has massively supported the building up of a PV manufacturing industry, protected the market, and concentrated global production in the region. When solar energy changed from a relatively expensive niche product into a mass consumption product, many European and US producers could not follow the price drop initiated by Chinese producers and went into bankruptcy. Even the recently imposed US trade tariffs on solar imports will not change the market structure, but rather will briefly slow down the installation of solar panels in the US.9

The effects of the solar boom on international politics are just beginning to emerge and can only be roughly sketched. However, a few preliminary conclusions can be drawn:

First, the availability of PV as an alternative to electricity generated by diesel engines could give a big push to development policies, especially in Africa and Asia. Today, only 30 per cent of Africans have reliable access to electricity.10 Electrifying rural areas, which now seems possible, would make many other development goals easier to achieve: access to clean water, independent economic activity, the use of electric appliances in general, or access to independent information via communication technologies.11 The emancipation of poorer social classes could fundamentally change the political landscape in many developing states, leading to a redistribution of political and economic power. In the future, it will be more difficult than ever to control the media and access to information, as the example of the “Arab Spring” has demonstrated quite clearly. The effects of such a development can hardly be predicted from today’s perspective and might be very different from country to country.

Second, the dominance of Chinese producers in PV manufacturing will not only bring economic benefits to the country. China will also be able to offer integrated clean energy solutions as part of its foreign policy, as is already the case with respect to other infrastructural developments, such as transport infrastructure. One of the crucial questions in this context is whether other manufacturers will be able to compete in the mass production of PV for the world market in the long run, given the competitive advantage and strong government support that Chinese suppliers enjoy today. With integrated supply chains for raw materials in the manufacturing process of PV, Chinese manufacturers might also have an advantage. The worries about conflicts over raw materials such as silver, copper, or some of the rare earths might be exaggerated in the sense that there will necessarily be a scarcity-led securitization of such resources. However, it is also clear that the Chinese government supports companies in accessing reserves, while creating political and economic pressure on countries with such resources. In addition, a high degree of local availability within China is also a clear advantage on global markets.12 Certainly, no material is without alternative; however, it will take years to develop technologies for producing PV hardware without some of the crucial raw materials used today and to scale production up for global mass distribution. The advantage enjoyed by the Chinese solar manufacturing industry will be very hard to beat for a long time, making the shift to solar good business for the country.

Third, the integration of ever more solar energy into the electricity systems all over the world will put grid operators and national electricity companies under stress. On the one hand, they will be forced to invest in additional measures to maintain high levels of system stability. On the other hand, they will lose revenues if they do not own solar capacities themselves. In some economically more developed states, this will eat into the revenue streams of electricity suppliers and force them to either charge customers more in order to finance their fossil investments or take political measures to keep solar off the grid. Especially in the case of state-owned utilities, this conflict is only now beginning to appear on the political scene.

So far, the development of solar energy has been very heterogeneous on a global scale, with only very few countries generating more than five per cent of their electricity from solar. China is, however, leading in absolute terms when it comes to producing and installing solar energy. Especially in developing countries and emerging economies, additional solar investments might only cover additional electricity demand, but not compete directly with incumbents on existing market shares. This also means that the challenges will be different in different world regions and on different scales of economic prosperity. It is clear, however, that global commitments to limiting global warming will not be met without a massive expansion of investments in solar all over the world. With the ability of individual consumers to buy solar installations and use them in many different circumstances and for different purposes, the traditional model of state-controlled electricity supply is likely soon to become obsolete. The solar revolution has just began.

The Battery Revolution: Ready for Take-off

The ability to store electricity on a large scale has long been one of the big dreams of mankind. Storage options would make the complex balancing of supply and demand in electricity systems easier and advance the use of electricity as an energy source for more applications in everyday life. Of course, in some places, electricity storage is already far developed. Switzerland’s hydropower infrastructure with its fleet of pump-storage installations is one example. So far, many states have relied on storing fossil fuels in large quantities instead of expansive storing of electricity. This situation is likely going to change.

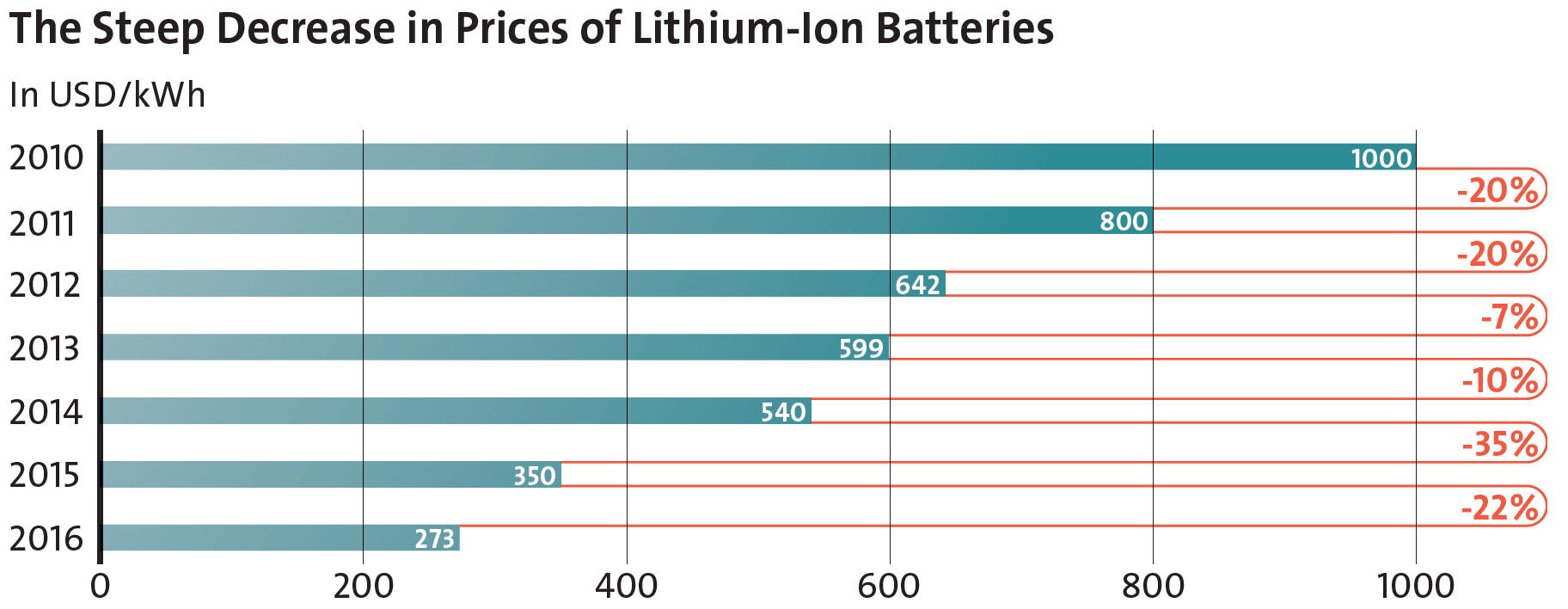

This change is already becoming apparent on a smaller scale when we look at the battery technology of the smartphones in our pockets. However, first promising changes are visible on a larger scale too. In the case of electric vehicles, whose main innovation is the battery technology installed, battery costs have decreased remarkably over the last years. Since 2010, the price for a battery pack has declined by 80 per cent, mainly due to productivity gains achieved by Chinese manufacturers, reaching 227 USD per kWh in 2017, according to a recent McKinsey study.13 So far, public attention has mainly focused on lithium-ion batteries, but other battery or storage technologies could become prominent as well in the future. Up to now, the race to find the best technology for electricity storage has not yet been decided, but lithium-ion is clearly in the lead when looking at costs, efficiency, and today’s production levels for all different purposes – in IT, but also in the automotive industry.

One common fallacy is the firm conviction that the rise of clean energy and the emergence of batteries must take place in a synchronous fashion. It is clear that in a world based on renewable energies only, electricity storage would necessarily have to play an important role. Without storage options, extraordinarily high capacities of intermittent renewable energy would be required and large-scale cross-country trade would be inevitable. At the same time, batteries could start to gain market share even with zero or only moderate development of clean energy, as a way of meeting within-day changes in demand. This independent development can also again be demonstrated in the case of electromobility, one example being Poland, where the government is making great efforts to extend electromobility, while at the same time, the electricity mix will be dominated by coal for the foreseeable future.14 Therefore, deployment of electric mobility is not necessarily coupled with clean energy development, but could also happen in a fossil- or nuclear-dominated world.

At the same time, the issue of batteries is not limited to transformation in the transport sector only. The use of batteries in microgrid systems is at least as important. These systems could either be communal or industrial facilities that see an opportunity in organizing their energy system individually, independent of state electricity suppliers. A recent Navigant study estimates that investments in microgrids will reach up to 100 billion USD over the next decade.15 This again shows that there is in fact a business case for the solar revolution to go hand-in-hand with a battery revolution. Independent deployment, however, is a plausible scenario as well.

So far, industrial battery development is primarily enforced by only a couple of states. Again, China plays a dominant role. Only recently, China’s battery company CATL announced a huge 2 billion USD investment in the world’s largest battery factory.16 South Korea has also joined the group of early movers. For the production of batteries, access to raw materials will be even more essential than for PV. Especially lithium carbonate and cobalt could be crucial in that respect. The crux of the matter is their geographical concentration within just a few countries. African states such as the Democratic Republic of the Congo with its large cobalt reserves are among the key staging grounds for the competition around cobalt and other raw materials. On this level, China has already worked on finalizing long-term trade deals, guaranteeing steady supplies.17 While in the coming years, the efficiency in the production of batteries could be slowed down due to a massive increase in raw material costs, as is already the case with cobalt, which experienced a price increase of 129 per cent in 2017, the real challenge is a different one. Again, when we consider the market for electric mobility, China’s dominance becomes apparent. China represents half of the global market for electric cars. The development of batteries and the construction of appliances with storage elements is part of China’s industrial strategy, with highly successful implementation in the first stages. Chinese companies are engaged in every segment of the supply and value chain for batteries and electric vehicles, making it very difficult for outsiders to access this market.18

Source: Claire Curry, “Lithium-ion Battery Costs and Market”, in: Bloomberg New Energy Finance (2017), 2.

To be clear: The widespread use of batteries is not a reality yet and has only started. Electric cars are still a marginal product on a global scale, and microgrid systems are in an early stage of deployment. However, there are many signals indicating that the next decade will see an extended use of different storage options and a massive increase in investments, first and foremost in batteries. This will individualize electricity supply to a high degree, especially in combination with renewable energies. At the same time, a proliferation of storage devices would reduce investments in electricity generation capacity, since peak load would be satisfied with storage and demand side management, rather than with additional generation capacity. All of this will also have implications for international politics.

First, the transport sector will be affected by the technological advancement of battery use for e-mobility. The market shares of European and US car manufacturers, which form an important part of the economies on both continents, are being challenged by cheap Chinese alternatives. In the next step, buses will also switch to electric power, although it will be difficult to produce sufficient storage elements for an increasingly electrified transport sector. The changes in the manufacturing of transport vehicles in general will massively impact the economic balance on a global scale and most likely hurt employment in the Western world. If the industrialized countries of Europe and North America fail to develop a way to compete with Chinese dominance, the battle for batteries will be lost, just as the battle for solar has already been lost. However, in this case, the impact will be much more drastic.

Second, not only in the case of PV, but also in the case of battery technology, Chinese competitive dominance will become apparent. Chinese companies will be able to offer integrated solutions for micro-grids and other storage options, including batteries. They could generate particularly attractive business cases through cooperation with solar manufacturers, offering one-size-fits-all solutions to countries. There is a great risk that China will monopolize investment in the transition to clean energy, especially in the developing world. This could also have an impact on political dependencies and strengthen China’s influence in the world.

Third, the spread of batteries and storage options will have an impact on the relationship between citizens, communities, and regions within states and even at the transnational level. Unlike in the 20th century, when the government controlled its citizens’ and regional entities’ access to energy, decentralized systems will make these actors become more independent. In this scenario, the state loses control, which could, for example, benefit separatist movements politically and militarily. Also, in future conflicts, energy independence will be a strong asset for all parties that will be enforced by a technological gain in autonomy, a hot topic in military technology research for years. Under these circumstances, warfare too might change due to the combined introduction of solar and battery technologies.

Political Implications

In the past, the role of energy in international politics was predominantly a hydrocarbon issue. Control over, access to, and prices for oil and natural gas were considered important factors in international relations. This period is most likely ending, for several reasons. One is the abundance in the hydrocarbon sector; another is the increasing role of renewable energies. When considering global investments in the energy sector, hydrocarbons have already taken a back seat. Industrial policy, trade, and environmental issues are becoming more important for geopolitics as well. However, there are some important caveats to this observation.

First, global energy demand is still rising and will continue to rise years, if not decades to come. The most recent BP Energy Outlook 2018 predicts an increase by one-third by 2040.19

Emerging economies and developing countries in particular have growing populations that are increasing their consumption of goods, products, and services. If no drastic energy efficiency and climate policy measures are introduced on a global scale, the hydrocarbon world will stay. Second, the electricity sector will be the first to be affected by massive changes. Already today, there are more and more renewable energies being introduced into the electricity system, where they compete with coal, gas, and nuclear for market shares. As we can see in China, however, growing electricity demand means that all energy sources will be needed, limiting controversial competition between fuels. Nevertheless, China is serious about integrating renewable energies in order to limit environmental damage and pollution, but also in order to slow down the increase of its massive energy trade deficit. Third, although the transport sector is changing, this will not fundamentally affect oil consumption in the short to medium term, at best leading to a slight abatement of still growing demand. Individual mobility only accounts for around a third of the world’s thirst for oil. With electromobility gaining some percentage points in market shares here, the overall picture for oil consumption is not going to change quickly. Overall, this means: Technologies are swiftly entering markets, and progress is accelerating quicker than most people would have thought, but fundamental changes on a global scale will only happen if global energy demand remains steady or begins to decline.

When considering the effects of the three breakthrough technologies, we need to take a sectoral and regional approach. The emergence of hydraulic fracturing had mainly an impact on the hydrocarbon side of the global energy system. Thanks to the US “energy dominance” paradigm, global commodity markets for oil and natural gas are flooded with cheap North American products. This has caught many fossil fuel suppliers by surprise and forced them to cut back on investments and public spending. The trend has also emphasized that the hydrocarbon age is most likely not going to end because of limitations to the availability of oil and gas. Its demise will rather be a process driven by technological substitution, economic efficiency, and environmental considerations in the long run. As some fuel-exporting states are already trying to change their business models, growing production is likely to keep prices and revenues at low levels for the foreseeable future, also constraining the states’ ability to finance transformations. However, with the emergence of relatively small private producers from liberal economies with a technology that has the potential to spread further internationally, global commodity markets will be less dependent on single suppliers and generally more flexible. This might also bring some degree of volatility.

While the hydrocarbon world is still dominant in the global energy system, the growth of renewable energies that has already been underway for years recently reached an important benchmark: comparable cost levels in electricity production. The most impressive development in terms of cost-efficiency, productivity, and learning curves in general has been in the case of solar energy, most notably PV. The fact that PV is easy to install and can be bought by individuals has contributed to its success. Together with the development of batteries in an integrated system, this technology offers a great chance to boost development in the peripheries of Sub-Saharan Africa and Asia. In general, the development of solar (with or without storage options) will help decentralize energy supply structures, with economic and/ or political effects for the centralized state and its domestic interests in many regions of the world.

The US and China are thus the political winners in two different games in town, confirming a trend towards a bipolar world order that we can also observe in other policy areas. The US wins because the battle for resources is not as relevant anymore (if it ever really was) and the trade deficit can be lowered massively by exporting oil and gas in the future. While political discussions around energy studies usually focus on the effects on the overall system and the end-consumer of energy services, the development of PV and batteries will mainly be driven by factors such as technology access, competition, and industrial policies. Clearly, based on investments and market shares, China is trying to dominate the market for both products. If the US, Russia, and the Middle East are the resource centers of the hydrocarbon world, China is on its way to becoming the monopolist of the future clean energy world. Despite the positive impact of making technologies available on a global scale, the implications for competition, access to these technologies, and the supply of raw materials will be important issues for future discussions on the geopolitics of energy. In this context, it seems that Europe is straddling both worlds: It is largely import-dependent on fossil fuels, while at the same time pioneering a revolution in the energy system, but unable to keep large shares in a clean energy market that is more and more dominated by China.

Notes

1 Daniel Yergin, The Price. The Epic Quest for Oil, Money and Power (New York: Simon and Schuster, 1991), 11 – 15.

2 R.L. Kleinberg et al., Tight oil market dynamics: Benchmarks, breakeven points, and inelasticities (Energy Economics 70, 2018), 70 – 83.

3 Kleinberg et al. (2018), 76.

4 Severin Fischer, “OPEC and Strategic Questions in the Oil Market”, in: CSS Analysis in Security Policy, No. 216, 11.2017.

5 Cf. Sarah Ladislaw, Dissecting the idea of US energy dominance (The Oxford Institute for Energy Studies, forum No. 111, 11.2017), 5 – 8.

6 Cf. Meghan L. O’Sullivan, Windfall: How the New Energy Abundance Upends Global Politics and Strengthens America’s Power (New York: Simon and Schuster, 2017); Meghan L. O’Sullivan, US energy diplomacy in an age of energy abundance (The Oxford Institute for Energy Studies, forum No. 111, 11.2017), 8 – 11.

7 International Energy Agency, Renewables 2017. Analysis and Forecast to 2022 (Paris 2017).

8 Cf. IEA 2017.

9 Salvador Rizzo, “Trump says solar tariff will create ‘a lot of jobs.’ But it could wipe out many more”, in: The Washington Post, 29.01.2018.

10 Charlotte Auban, “Accelerating Africa’s Energy Transition” in: Project Syndicate: The World’s Opinion Page, 11.01.2018).

11 Jatin Nathwani, “Empowering the powerless: Let’s end energy poverty”, in: The Conversation, 29.01.2018.

12 Meghan O’Sullivan/Indra Overland/David Sandalow, The Geopolitics of Renewable Energy (Working Paper, Columbia SIPA/Belfer Center/ NUPI, 06.2017).

13 McKinsey&Company: Electrifying insights: How automakers can drive electrified vehicle sales and profitability (Advanced Industries, 01.2017).

14 Interview by Frédéric Simon, “Polish exec: Electro-Mobility Act creates whole ecosystem for EVs”, in: Euractiv, 09.02.2018.

15 Navigant Research, Microgrid Enabling Technologies Market Overview (2018).

16 Karel Beckmann, “Chinese CATL soon biggest battery maker, Europe far behind, can grid cope with EVs? “, in: Energy Post Weekly, 06.02.2018.

17 Thomas Wilson/Thomas Biesheuvel, “Electric Cars and Niche Metals Lure Cash to Africa’s Mines”, in: Bloomberg, 02.02.2018.

18 Scoot Patterson/Russell Gold, “There’s a Global Race to Control Batteries – and China Is Winning --- It’s locking up the supply chain for cobalt, essential to lithium-ion batteries”, in: Wall Street Journal, 11.02.2018.

19 BP, BP Energy Outlook 2018 (London 2018).

About the Author

Dr Severin Fischer is a fomer Senior Researcher at the Center for Security Studies (CSS) at ETH Zurich. He currently works for the German Federal Ministry for Family Affairs, Senior Citizens, Women and Youth.

For more information on issues and events that shape our world, please visit the CSS Blog Network or browse our Digital Library.

No comments:

Post a Comment