By Gordon Orr

The nation could be shaped by geopolitics, momentum from robust economic growth, and a host of new leaders eager to implement new policy. With so many new leaders put in position over the last six months by President Xi, an overall leader secure in his position and clear on his objectives, 2018 is likely to see much more activity to implement policies, economic and social, that move China in the direction that Xi wants. We may need to worry more about overenthusiastic implementation of policy than the inaction we have often seen in 2017.

Again, the year could well be shaped by geopolitical discontinuities. Opportunities for Chinese companies to invest overseas have diminished in a number of markets, but as of yet, opportunities for trade have not been materially restricted by the governments of importing countries. Relations with Japan and the United States remain volatile, with the potential for damaging discontinuities in trade and investment.

Yet China enters 2018 with robust economic-growth momentum. Despite stresses that we highlighted last year, which have only grown—regional disparities, an aging population, declining heavy-industrial sectors, property bubbles, growth in debt levels, and continuing environmental pollution—China remains slightly ahead of track of its goal to double GDP between 2010 and 2020 and to realize its self-declared ambition to become a “moderately prosperous” country.

Given this, how might 2018 unfold?

China’s continued international expansion—with bigger bumps in the road

After a pause and reset to eliminate outbound investment that the government found frivolous, China Inc.’s outbound investment will resume its upward trajectory in 2018, with a focus on Manufacturing 2025 sectors and Internet-enabled businesses, such as artificial intelligence (AI) and the Internet of Things. Many global-scale Chinese companies are still mostly focused in China, and they are impatient to scale elsewhere. The reality is that even in 2017, China’s more mature outbound investors kept moving ahead with strategically relevant investments ranging from computers, aviation, and automotive to wealth management, schools, and healthcare. Many of these more mature investors already have businesses outside China of the scale of a Fortune 500 company, with the ability to raise cash where they need it for investment. Geographically, Brazil, Japan, and the United Kingdom in particular saw increased interest. In 2018, investment in these sectors will continue with a particular emphasis on the service sectors—healthcare, tourism, education, gaming, and similar.

The international reach of China’s tech companies and investors grew and grew with myriad, often minority, investments too small to show up in national statistics but that gave companies access to innovative technology and business models to scale in China. In 2018, a lot more attention will be paid to global Chinese investment in these fin-, med-, and edtech and AI start-ups, with political pushback in the United States, leading them to focus more heavily on Israel, Scandinavia, and the United Kingdom. De facto, many Chinese investors will simply assume that they could not get approval for investment in the United States and so won’t try. If US–China economic relations deteriorate significantly, we even might see real pressure to break up deals consummated in years past.

Belt and Road will remain the flagship international state-to-state collaboration program for building China-sponsored infrastructure around the world. In 2018, there will be more scrutiny of projects, potentially leading to delays (as with the high-speed rail links in Eastern Europe) but also more projects under way. While in part this will be a result of rebranding existing work under Belt Road, clearly the heads of relevant state-owned infrastructure companies are under strong pressure to deliver real projects as central government in Beijing has become frustrated at the slow pace of project realization. In 2018, multinationals should focus more on what business opportunities result from a port in Kenya, railroad in Hungary, or industrial free-trade zone in Kazakhstan than on gaining a major slice of the construction work.

Beyond supporting its businesses to expand internationally, China’s government will grow its soft-power initiatives in 2018, investing more in its Chinese culture centers at universities around the world, in its international media projection online and on traditional TV, and through its official overseas development-aid budget, the largest recipient of which in recent years has been Cuba.

Domestic centralization and control

A strong, powerful leader with a team around him largely selected by the leader are common ingredients for more centralization for economic decision making and control. China is no exception. And economic success over the last five years, relative to the rest of the world, has created confidence that the government can micromanage at the sector level successfully. But there are additional reasons why China will be visibly more centrally controlled in 2018.

In the financial sector in particular, regulators have moved beyond making examples of individuals whose actions they disapproved of, to a much clearer and complete set of regulations of what is permitted for wealth-management companies, insurers, and online financial-service providers, massively restricting opportunities for regulatory arbitrage. Areas of ambiguity that were large enough in the past, for example, allowed Internet players to become highly popular asset managers and key payments providers without a license. By 2019, it may be hard to even launch small incremental services without approval. Specifically in payments, all online payments will now have to pass through a central government-run clearing house, so that the government can now, should it choose, see who is passing money to whom. Clearer regulation is not a bad thing per se, many multinationals have complained for years that they could not invest with certainty due to ambiguity over regulation. We can hope that the data-protection and cybersecurity laws become similarly clearer in 2018.

Would you like to learn more about McKinsey Greater China?

After years of failed exhortation to local government to enforce demands that it cut capacity in traditional heavy industries such as coal, steel, and chemicals, the forces of China’s centralized anticorruption agency have been unleashed to root out recalcitrant behavior. With the soon-to-be-established super-anticorruption agency, the National Supervision Commission, Beijing will have an easier time rooting out local noncompliance and making an example of officials and executives. Existing anticorruption agencies will be consolidated under the commission, which will oversee inspections of all government departments, state-owned firms, and institutions.

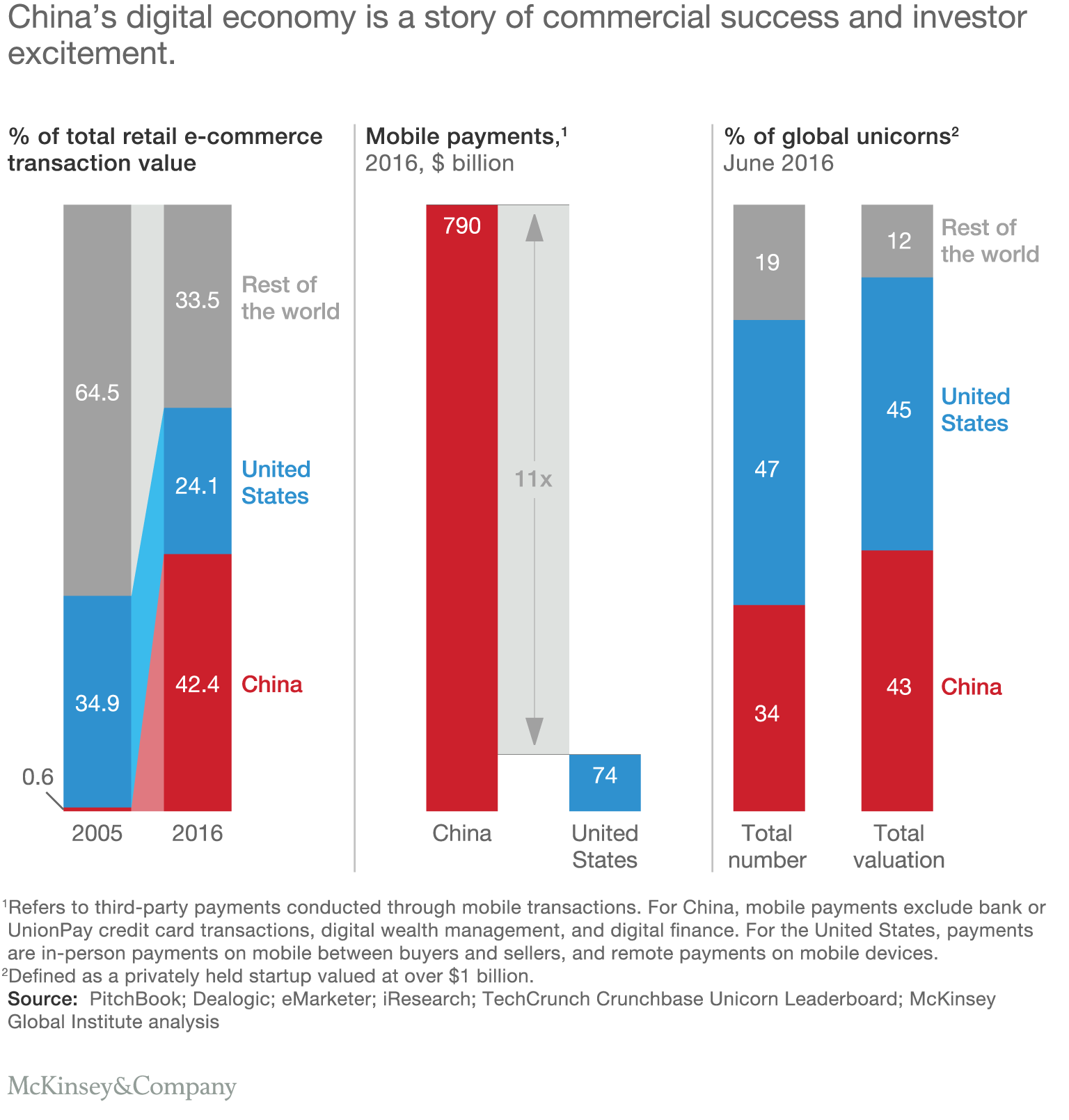

The success of China’s technology giants is another reason why greater control is possible (Exhibit 1). Creating such popular online payments that cash will become obsolete in China by 2020 (they are already the majority of retail payments) means that financial flows are easier to monitor. Requiring real-name usage for any activity on the Internet allows similar oversight of online behavior.

Exhibit 1

And in the physical world, facial-recognition technology has progressed to the level that Tencent can work with public security bureaus to identify children stolen from their families, even years after the event, by projecting how their facial characteristics will evolve and picking them out when they appear on CCTV in a public area or online. Indeed, visit one of the solution-demonstration areas at leading high-tech companies in China and you will see how smart cities using AI on government, business, and individual data is already being realized at scale today.

Domestic industry tipping points in 2018

As ministries become more active in 2018, industries such as retail will see a continuation of long-term trends, Internet-based businesses will continue to attract the most attention, and a number of other industries could reach key tipping points.

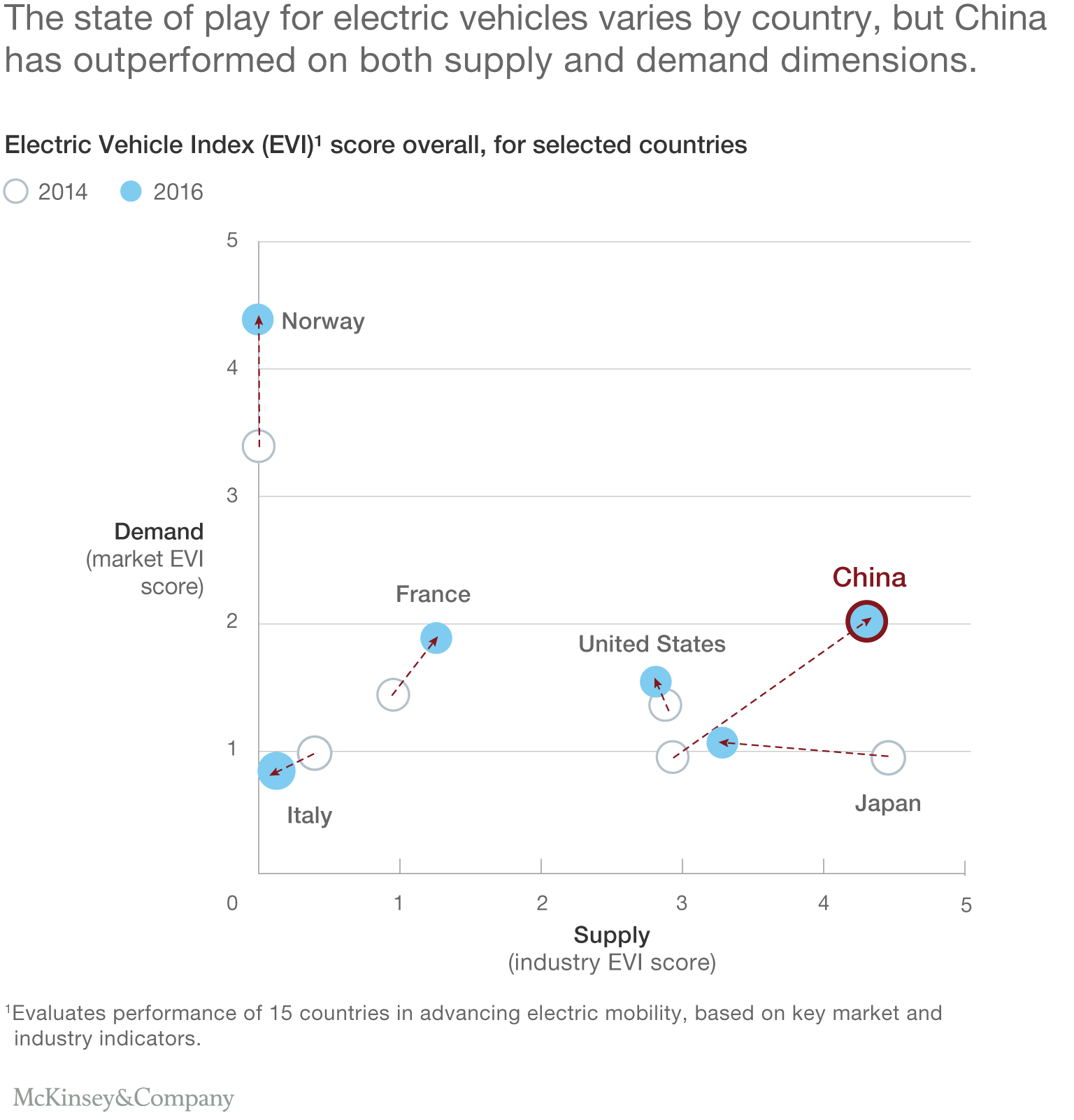

Automotive. Regulations in the auto sector require manufacturers to dramatically increase sales of electric and near-electric vehicles every year for the next several years. One set of regulations focuses on the share of new-energy vehicles versus traditional combustion-engine vehicles an OEM produces. If they fall short, they need to purchase offset carbon credits. A second regulation focuses on the fuel efficiency of the fleet sold. This is all part of fulfilling the government’s ambition to dominate the global electric-vehicle (EV) market by 2030 (Exhibit 2).

Exhibit 2

In addition to regulation, more than $50 billion in subsidies will be given to the industry by 2020. BYD and CATL, China’s two leading battery producers, are aggressively hiring talent from South Korea and the United States to enhance their development capabilities. Power-grid companies have installed nearly 200,000 charging stations.

Cities like Shenzhen have switched all their buses to electric, and taxis will be next. Other cities that restrict the sales of license plates have made an exception for EVs. Global OEMs are not planning to lose the lucrative China market that has driven their global profit growth for many years. Volkswagen, for example, has committed to a $10 billion-plus program to develop EVs in China—2018 has to be the year when OEMs and the government together crack creating true market demand. If they do, China will indeed be on a path to achieving its long-term EV ambitions.

Pharmaceutical. Major regulatory changes at the China Food and Drug Administration to modernize drug approvals led to more than 35 major new launches in 2017 (versus only five in 2016), most from multinational companies (MNCs). This higher rate will continue. And more than 300 drugs were added to the National Reimbursement Drug List. More drugs in the market, more drugs reimbursed, more patient access through online services, and more funding from billions of dollars of private-equity and venture-capital funding supplemented by true innovation by Chinese companies. In biotech, Chinese companies have more than 800 molecules in the development pipeline and are aggressively licensing in and out of China. They also invested billions of dollars for the first time in outbound M&A—not just in biopharma but also in healthcare services and med tech start-ups. China’s tech and finance leaders, such as Baidu, Ping An, and Tencent, are launching AI and big data–based innovations, working with local government and hospitals to create better patient outcomes. MNCs are also able to play a leading role. Bristol-Myers Squibb, for example, launched China’s first outcomes-based insurance program for hepatitis C patients in partnership with Shanghai Pharma and Huatai. The era of pushing drugs through sales agents to doctors to be massively marked up by hospitals for sales to patients is ending.

Steel, cement, and coal. In 2018, we should finally see these industries realize that their future is to shrink year on year for the decades to come, as they enter a mature stage that we saw in Western markets 20 to 30 years ago. More effective regulation of output volumes, of days of production, of pollution output, and of capital investment will genuinely reduce output, rather than the very soft reductions we have seen in prior years. State-owned enterprises will be further consolidated in 2018, their surplus capital given as dividends to the state, especially important now that state pension funds hold 10 percent of their shares and rely on the dividend for funds flow. Aging workers will be retired out and actual layoffs are being supported. The good news for the remaining, hopefully large-scale higher-quality companies, is that they could see a virtuous cycle develop and sustain in 2018—less capacity, fewer competitors, a more orderly market, higher prices, higher profits, higher dividends, and happier owners. Exports will still be used as a release valve, causing disruption in markets that remain open to Chinese steel imports.

Pensions and asset management. The establishment of the Financial Stability and Development Committee in 2017 will really translate into market impact in 2018. Shadow banking will be severely curtailed. Online microlending likewise. Consolidation and reconcentration of assets into the largest institutions is possible. High-yield investments in products that investors saw as risk free but that were not (such as many wealth-management products issued by insurers) will be curtailed. Trillions of dollars of assets will be looking for return in new areas, potentially rapidly expanding the $1.7 trillion public mutual-fund market. There could be many beneficiaries—wealth managers, asset managers broadly, and mutual-fund managers specifically (especially active fund managers), as well as the big four banks. China’s fund-management sector is already doing extremely well; in the first half of 2017, net margins were greater than 30 percent. Overlay on top of this increased opening to foreign involvement in the financial sector, especially in wealth management, and competition could intensify fast.

E-sports, not soccer. For soccer, 2018 will be a much quieter year for Chinese investment. And from Italy to the United Kingdom, last year’s soccer entrepreneurs are realizing that it is much easier to buy a soccer team than to run it successfully. In contrast, China’s e-sports players are driving the global industry. With more than 1,000 professional e-sports players in China, the top 20 each earned more than $1 million this year in competition prize money; sponsorships add much more. Tournaments and live streaming both are major revenue streams for the industry. With hundreds of millions of amateur players, and a huge appetite to follow the best players in the same games that the amateurs play, revenues (in a very poorly analyzed sector) appear to be rising well over 25 percent annually. China’s professional soccer teams have even fallen in with the trend, setting up an e-sports professional league. There is more chance they win the e-sports world cup than the soccer world cup anytime soon.

Capturing China’s $5 trillion productivity opportunity

Push for inbound investment

Greater Bay Area. As China’s economic center of gravity continues to move south, the emergence of the Greater Bay Area (GBA) as a coherent, coordinated development area has the potential to draw in a disproportionate share of China’s next wave of growth. Comprising Guangzhou, Shenzhen, and Hong Kong—along with other cities—to give a total population of 70 million, with GDP per capita of more than $20,000, the GBA has the headquarters of many of China’s most innovative start-ups and scale enterprises, a world-leading combination of hardware and software capabilities, and great depth of international financial resources. Demand for high-skilled blue- and white-collar workers is as high in the GBA as anywhere in China, reflected in rising wages and a parallel shift into more value added, more automated manufacturing sectors. The region’s population grew faster in 2000 to 2010 than any single province in China and has a median age five years below the northeast, giving it almost ten workers per pensioner. The demographic dividend that has played out in other parts of China is still working strongly in the GBA as a result of strong new inward migration. Local governments are working hard to retain these migrants permanently, making it easier for their children to register in local schools and to join local social insurance schemes.

In 2018, we will see if government leaders across the GBA can translate their local successes into action on a regional scale. If they do, then the attractiveness of this region to talent, investors, and businesses overall should create a reinforcing growth cycle based on 21st century industries.

Consumer wealth goes where in 2018?

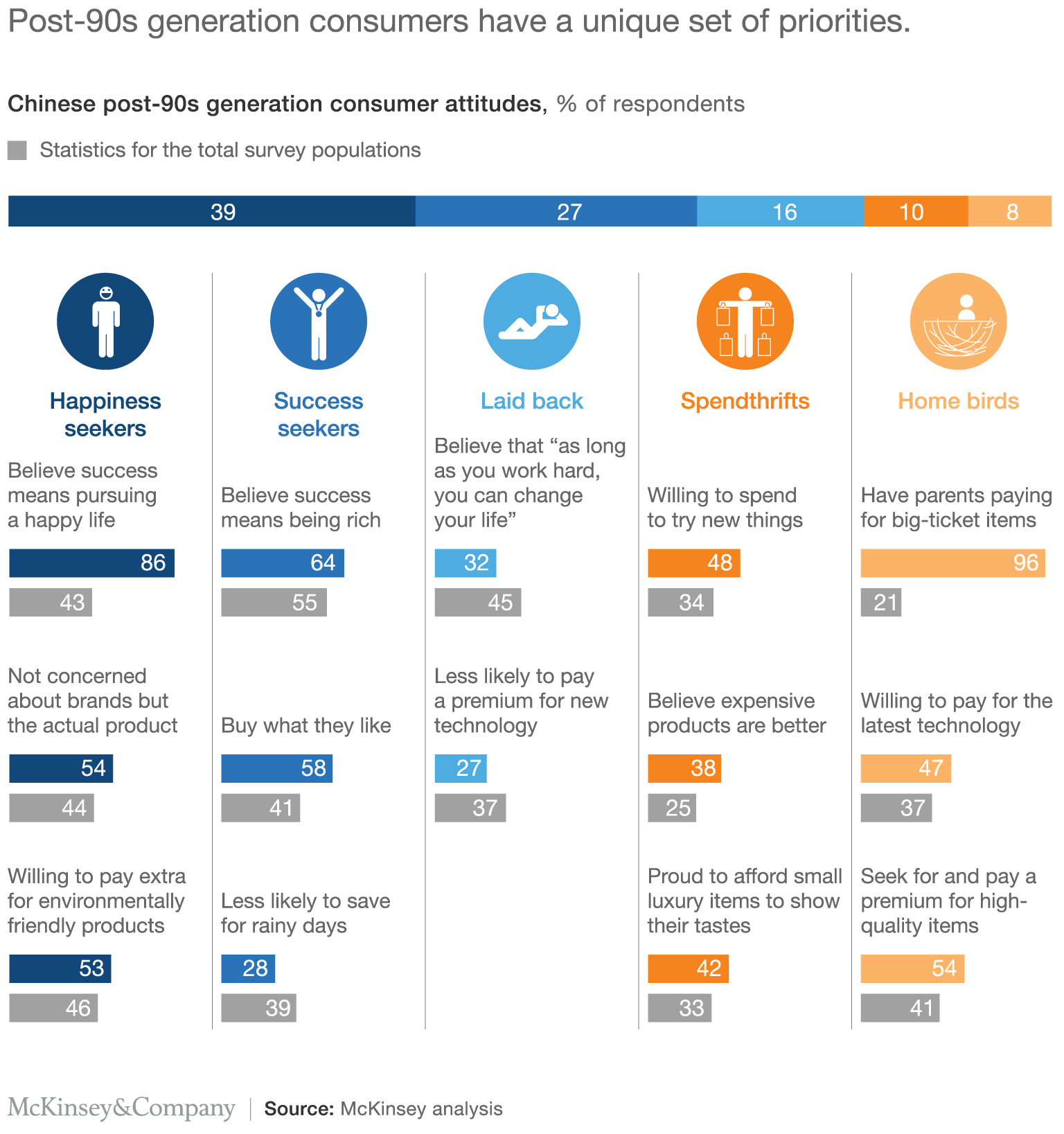

With inflation rising slightly and real disposable incomes rising 8 percent nationwide, consumers certainly have funds to save or spend. In aggregate, consumer spending will continue to grow in high single digits in 2018, backed by very strong levels of consumer confidence (also with wide regional variations). Spending will grow on health-related areas such as healthier foods, exercise activities, and medical expenses (for themselves and for elderly relatives). Increasingly, consumption growth will be driven by the generation born in the 1990s, a generation that has yet to experience anything close to a recession in their lives, and who have more balanced aspirations between achievement and enjoying life, versus prior generations who focused mainly on the former (Exhibit 3). The impact of this 1990s generation will become even clearer in 2018 as the group’s elders increasingly retire, shifting to lower levels of consumption. This is particularly true for northeast China and for China’s top-tier cities where fertility rates are below one.

Exhibit 3

The usual destination for China’s citizens’ savings—more property—has not proved as attractive in 2017, with only single-digit price rises nationwide and with the divergence across regions becoming ever wider. But at least there were no major cities where a bubble burst, sparing the government the need to intervene to bail out investors. With the government restricting access to mortgages and pushing the development of the rental market, this trend of more stable prices may become the norm. The stock market has also shown only 6 to 7 percent gains, but with a wide divergence between tech stocks and the rest. Many wealth-management products offered higher returns than this, but, as mentioned, their availability will be heavily restricted in 2018.

Even with consumption growth likely to continue in 2018, consumers will have more savings available. Where will they go? Individuals picking their own stocks to buy, and investing in active fund managers to pick stocks for them, will certainly be one area, and outbound investment through official channels into international stocks and bond markets another. And expect strong growth in private investment vehicles—more funds flowing to private equity and venture capital, inflating prices further. But even with this growth, there will be rising pressure through the unofficial channels to increase offshore investment in 2018.

Social priorities, real and acted on

The social priorities highlighted by President Xi at the 19th Party Congress are getting substantial attention already, with more to come in 2018. In particular, action on air pollution and poverty elimination will be priorities.

Pollution. More than 30 cities, mainly across northern China, have committed to reduce particulate matter (PM) 2.5 particle density by 15 to 40 percent over the winter versus last year. Heavy polluters are being closed for the season, some given money to upgrade their pollution-reduction equipment while they do. Older vehicles are being restricted from cities, and alternate-day license-plate limits imposed. Natural-gas supplies are being extended from urban areas into surrounding rural areas to substitute for coal burning. The actions required have been clear for years, and now we are seeing the commitment to take and sustain them. A good start, at least in Beijing, with PM 2.5 down 30 percent for October and November. The year 2018 will be about entrenching pollution-reducing actions as the new normal in these cities. Next needs to come action on cleaner water.

Antipoverty. As part of becoming a “moderately prosperous country” by 2020, the government is seeking to eliminate all areas of absolute poverty. In part, this will be done through transfers from the center, but much more will come from directing business, state owned and private, to invest either to bring services (such as the Internet) to these areas or to establish operations locally to employ people from the poorest areas. Whether delivered in response to a government instruction or proactively as part of a corporate sustainability program, capital will flow this way, and companies will hope to be recognized for their contributions. Provinces with clusters of poverty are becoming astute in pitching poverty alleviation as an element of why companies should invest with them. MNCs with scale operations in China need to develop plans for how they will engage on this government priority.

Overall in 2018 we should expect as our base case a year of slightly slower growth, with wider variations across provinces and cities than ever, driven by increased consumer spending skewed to wealthier cities and higher government social spending. This will be weighed back by lower property and infrastructure spending. Net exports remain the largest uncertainty in realizing economic growth, remaining subject to whatever actions the United States may initiate, perhaps initially on Chinese exports of tech goods but that could roll into multiple other sectors in a gradual escalation. Without this effect, we can look forward to a year of very positive developments in many sectors in China, framed by an environment of tighter and more centralized regulation and control.

No comments:

Post a Comment