Auguste Tano Kouamé and Habib Rab

Turkey, like the rest of the world, has been deeply impacted by COVID-19. This one-in-a-hundred-year crisis that has touched the populations of 216 countries, landed in Turkey in early March 2020. It jolted the Turkish economy just as it was starting to stabilize from a mid-2018 bout of turbulence. The question now is what should be the appropriate policy mix as the economy tries to navigate the COVID-19 shock and recover from the doldrum it has been in over the past couple of years?

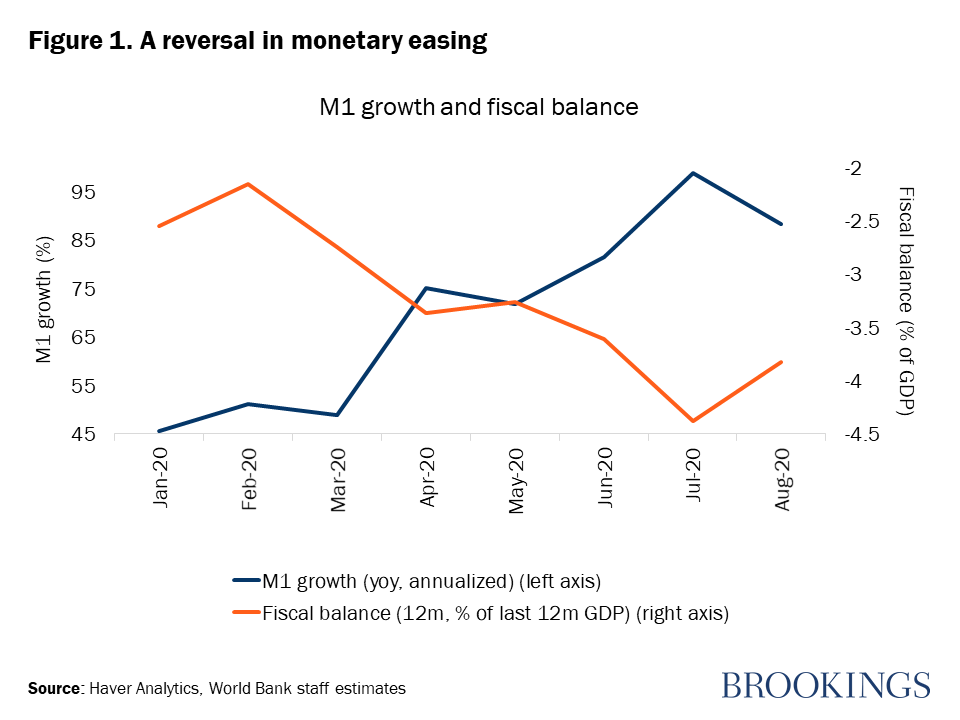

Turkey’s immediate response helped contain some of the more negative effects of COVID-19 though emerging economic imbalances have required policy tightening. Early social distancing, mobility restrictions, testing, and health capacity enhancements helped contain the spread of the virus and the number of fatalities. The economy came to a near sudden halt during the second quarter of 2020. Fiscal, monetary, and financial measures however extended support to some of the most affected parts of the economy. Leading indicators suggest that both supply and demand are making up for lost ground. At the same time, monetary expansion on the back of already negative real interest rates contributed to macroeconomic imbalances and an erosion of external buffers, eventually prompting a reversal in monetary easing.

These policy tradeoffs coupled with pandemic-related uncertainties present a range of possibilities for the economic outlook. We project the economy to contract in 2020 but the extent will depend on how the pandemic evolves in Turkey and among close trading partners, some of which are experiencing a second wave. The shock to household incomes could increase Turkey’s poverty rate from 10.4 to 14.4 percent, but the government’s existing policy response would likely decrease the poverty rate significantly from 14.4 percent to 11.5 percent. In a baseline in which the pandemic is brought under control by early 2021, economic growth could recover to 4 percent in 2021 and 4.5 percent in 2022.

Looking ahead, the challenge for Turkey will be to focus on sustaining macroeconomic stability and preparing for the long haul. This implies departing from a tradition of running sprints—namely stimulating short-term economic growth through credit stimuli—and preparing instead for a longer-term endurance race. This means securing macroeconomic stability and investor confidence. Recent statements by the newly appointed Minister of Treasury and Finance and Governor of the Central Bank seem to confirm that this objective will be prioritized. In a world where competition for external capital is likely to be fierce, a focus on macroeconomic stability could have positive payoffs in terms of capital flows, exchange rate stability, and lower risk premia.

To support this effort, Turkey can afford to maintain responsive and flexible fiscal policy to manage the recovery ahead. Turkey’s medium-term fiscal framework under different macroeconomic scenarios suggests that the country can absorb limited shocks even with the recent increase in fiscal imbalances. Thanks to the existing fiscal space—albeit declining—automatic stabilizers and targeted measures can play a role in shielding the economy from the COVID-19 shock. This can help avert significant social and economic costs, including widespread layoffs and insolvencies, and a permanent drop in lifetime earnings of households due to sale of assets and loss of human capital. The shock offers an opportunity to use some fiscal space to ensure that public spending on education can help improve learning outcomes and returns to human capital.

Balance sheet repair for corporations will also be needed to lay the foundation for investment recovery. Given the debt overhang resulting from pre-COVID credit booms and credit expansion during COVID-19, more credit is unlikely to sustain medium- to long-term growth. Corporate sector deleveraging is needed to prepare for a resumption in private sector investment when the world starts recovering from the crisis. This may require closer monitoring of current challenges to the banking sector’s health and supporting orderly deleveraging through corporate debt restructuring.

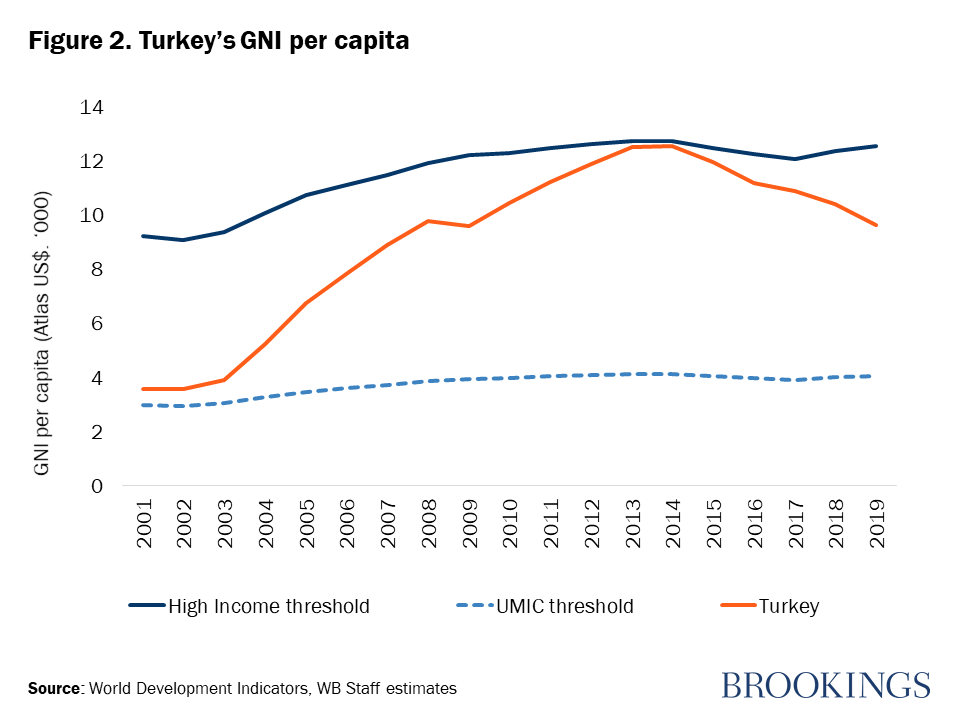

This crisis is an opportunity to refocus attention on structural reforms and build back a resilient economic system that propels Turkey into the high-income group of nations. Those reforms are captured well in the New Economic Program and the 11th National Development Plan. Deepening trade integration and participation in global value chains, accelerating labor market reforms, promoting innovation, diversifying the financial sector and enhancing access to long-term finance, and ensuring competition are a few priority areas to help boost the growth potential of the economy. These efforts, together with investments in human capital, should help reverse the drop in labor force participation including among women. Turkey nearly reached high-income status in 2014 thanks to a sustained period of growth supported by structural reforms in the preceding decade and a half. In order not to let a good crisis go to waste, the COVID-19 shock provides an opportunity to implement in earnest the structural reforms currently envisaged in various national strategic documents. This could allow the economy to repeat the sustained growth performance of the beginning of the 21st century.

No comments:

Post a Comment