Mika Kortelainen

In just over two months, the Russia’s war has caused severe economic dislocation in many areas. Ukraine’s economy has suffered immensely. The International Monetary Fund’s recently-released World Economic Outlook, for example, sees Ukraine’s GDP declining by a staggering 35 % this year. The war ultimately will be very costly also for Russia. General uncertainty has increased and sanctions levied against Russia have impaired domestic production as financing and foreign intermediate goods supplies have dried up.

In assessing the economic impact of Russia’s war, we utilize the global integrated monetary and fiscal (GIMF) model based on a general equilibrium framework (Kumhof et al., 2010). Our version of the model distinguishes three economic areas (Russia, the euro area, and the rest of the world), and includes oil production and oil prices as they are important in assessing the Russian economy.

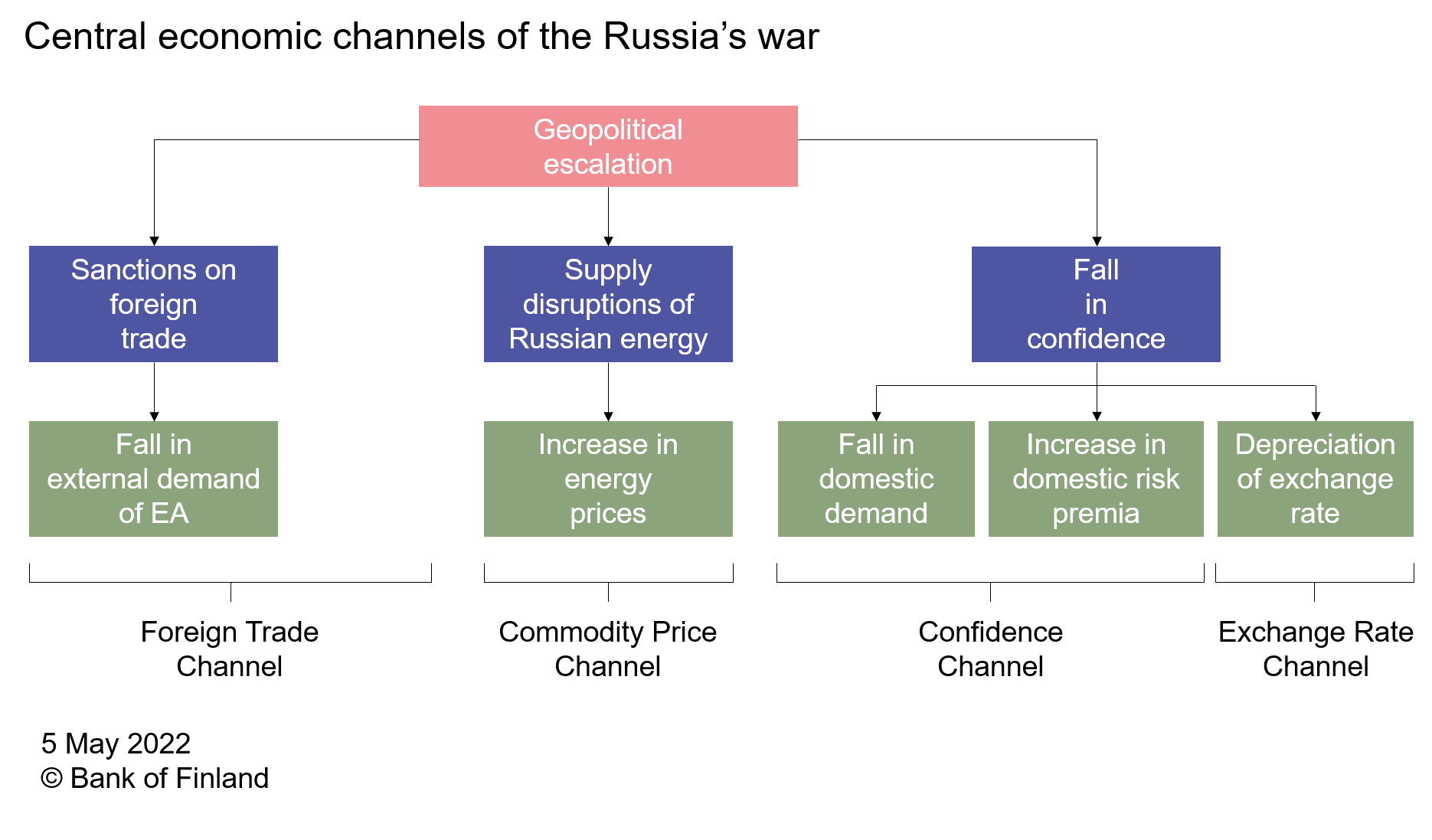

One way to think about the economic effects of the Russia’s war is to decompose them into different channels as shown in the Chart 1.Chart 1.

1

Scenario assumptions

In constructing a plausible multi-channel scenario, we make a few assumptions about shocks and responses to them:

Falling confidence works mainly through capital markets. We expect this effect to be most pronounced in Russia and to a lesser degree in the euro area. International investors sell off their Russian assets, leading to a roughly 30 % depreciation of ruble. To defend the external value of ruble, the Central Bank of Russia responds by increasing its policy rate by 10 percentage points. Despite the CBR’s prompt answer, overwhelming pressure against the ruble forces Russia to impose stringent capital controls to contain the capital outflow. The risk premium for Russian sovereign bonds rises by two percentage points and the corporate risk premium by two and half percentage points.

Households and firms in Russia and the euro area change their behavior. Specifically, we assume a change in the household’s discount rate that makes saving preferable to consuming. The increased user cost of capital to firms erodes the profitability of future fixed investments. Again, we expect that these effects are much stronger in Russia than in the euro area.

Global energy prices rise. This could be interpreted as a fall or a fear of future decrease in the supply of Russian energy (including both natural gas and oil). We assume the expected fall in supply increases the price of energy by 30 percent.

Russia counters euro area sanctions on imports in a tit-for-tat manner. These sanctions are modeled through tariffs and other trade impediments which are expected to double.

Overall, our model calculations suggest that decreasing confidence and higher risk premia, excluding the exchange premium,[1] reduce 2022 growth by about three percent in Russia and about one percent in the euro area. This is obviously just the first response of the economies, and the overall effects are larger, as outlined before.

Furthermore, caution is warranted with these results as the size and persistence of shocks in our scenario are uncertain. Moreover, the shocks likely interact.

Scenario results

The effects of the above identified shocks to Russian economy are shown in Charts 2 and 3, and the effects on the euro area economy are shown in Chart 4 below.

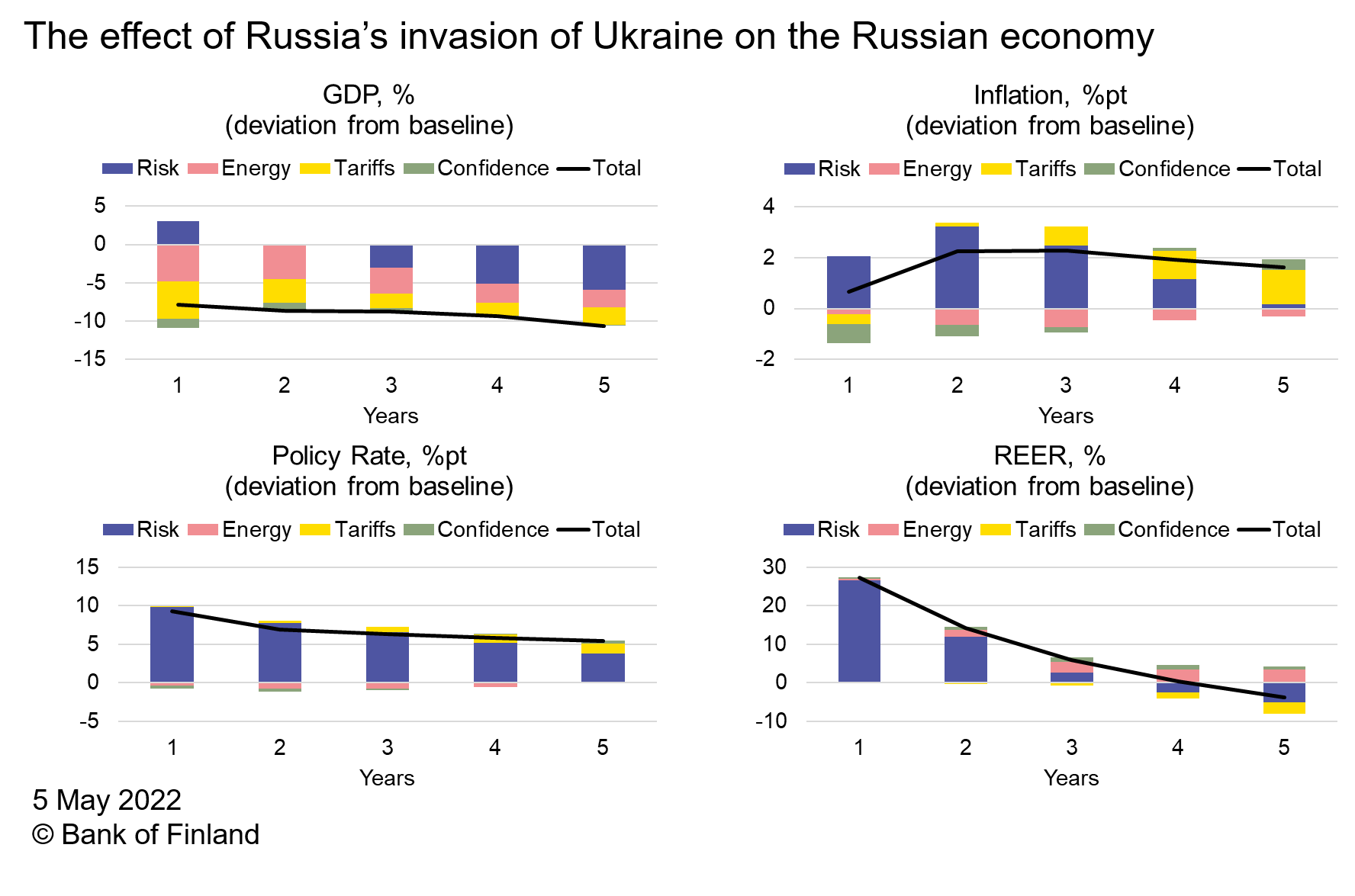

Chart 2.

The results in Chart 2 indicate that, due to the combined shock effects, Russia’s GDP falls by about 10 per cent and then remains at this depressed level for years. Inflation in Russia increases, but is kept to a modest increase of about 2 percentage points. This assumed increase in inflation could well be larger if the shocks are bigger or more persistent than assumed. Supply bottlenecks could also create inflationary pressure. Our assumed policy rate hike of ten percentage points corresponds to the observed initial policy rate increase from 9.5 percentage points to 20 percentage points by the CBR. The key rate presently stands at 14%. The ruble depreciates by 30 percent in nominal terms and almost equally in real terms (REER) against other currencies. This corresponds to the initial exchange rate reaction at the start of the war. The nominal value of the ruble has appreciated in recent weeks, mostly because the CBR introduced restrictions on currency markets, including a requirement that exporters convert at least 80% of their export earnings to rubles.

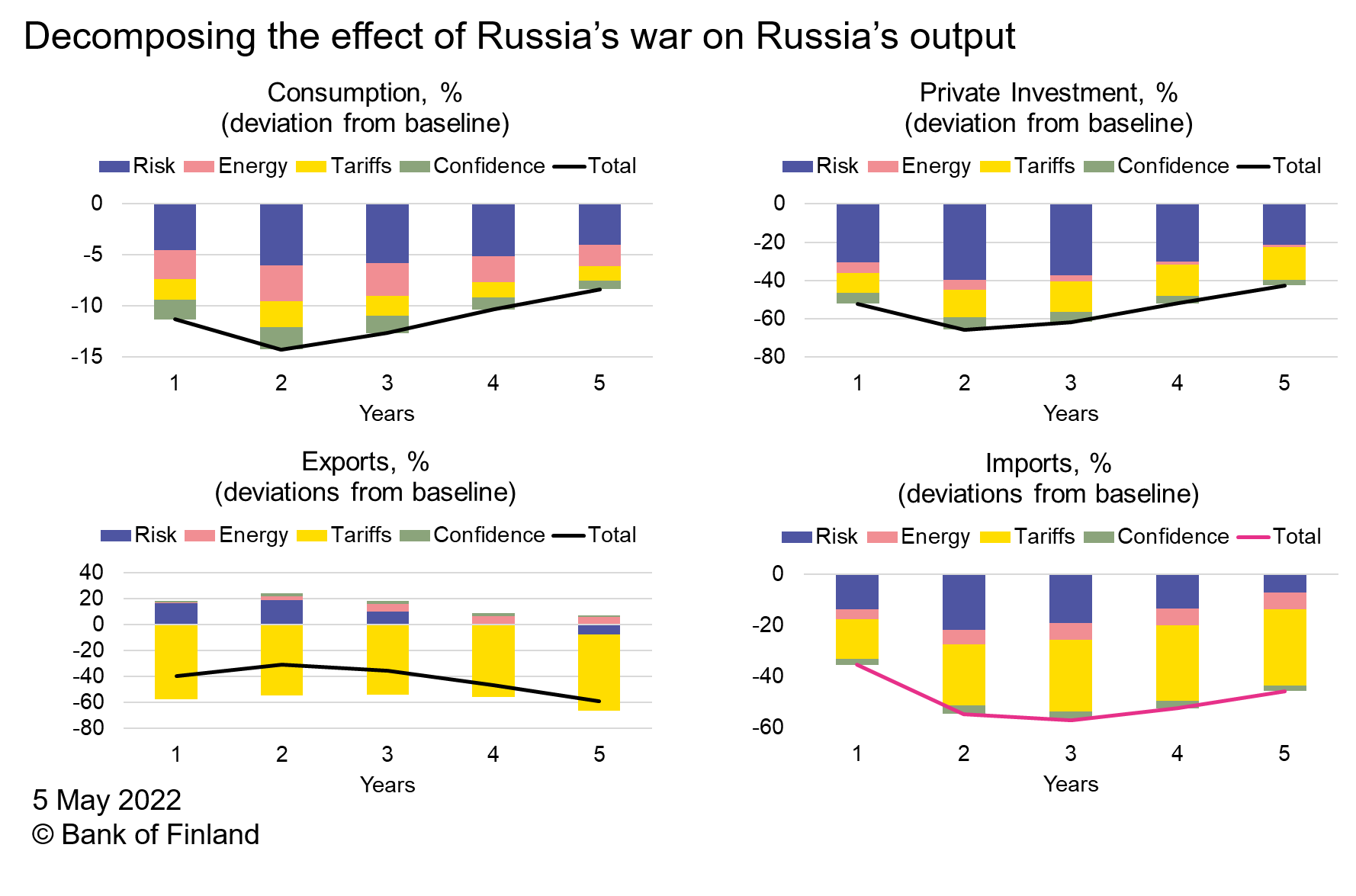

The fall in risk sentiment dominates the effect on Russian exchange rate, policy rate, and inflation. With respect to output the effect of different shocks is more even. Chart 3 contains a more detailed decomposition of the most important GDP components.

Chart 3.

Chart 3 shows that the sanctions on the foreign trade (tariffs) decrease both Russian exports and imports by roughly 50%. The export impact may be somewhat overstated as Russia’s main export is energy and the rest of the world faces a chronic negative net supply of the energy commodities provided by Russia. Even if Europe weans itself off Russian energy exports, demand in other markets remains in the medium term even with higher trading costs from longer transport distances. The fall in the private consumption is hefty 10-15 percent and the private fixed investment drops by nearly 50%. This drop in private fixed investment implies a lack of new capital investment in Russia with most fixed investment going to maintenance of the existing capital stock.

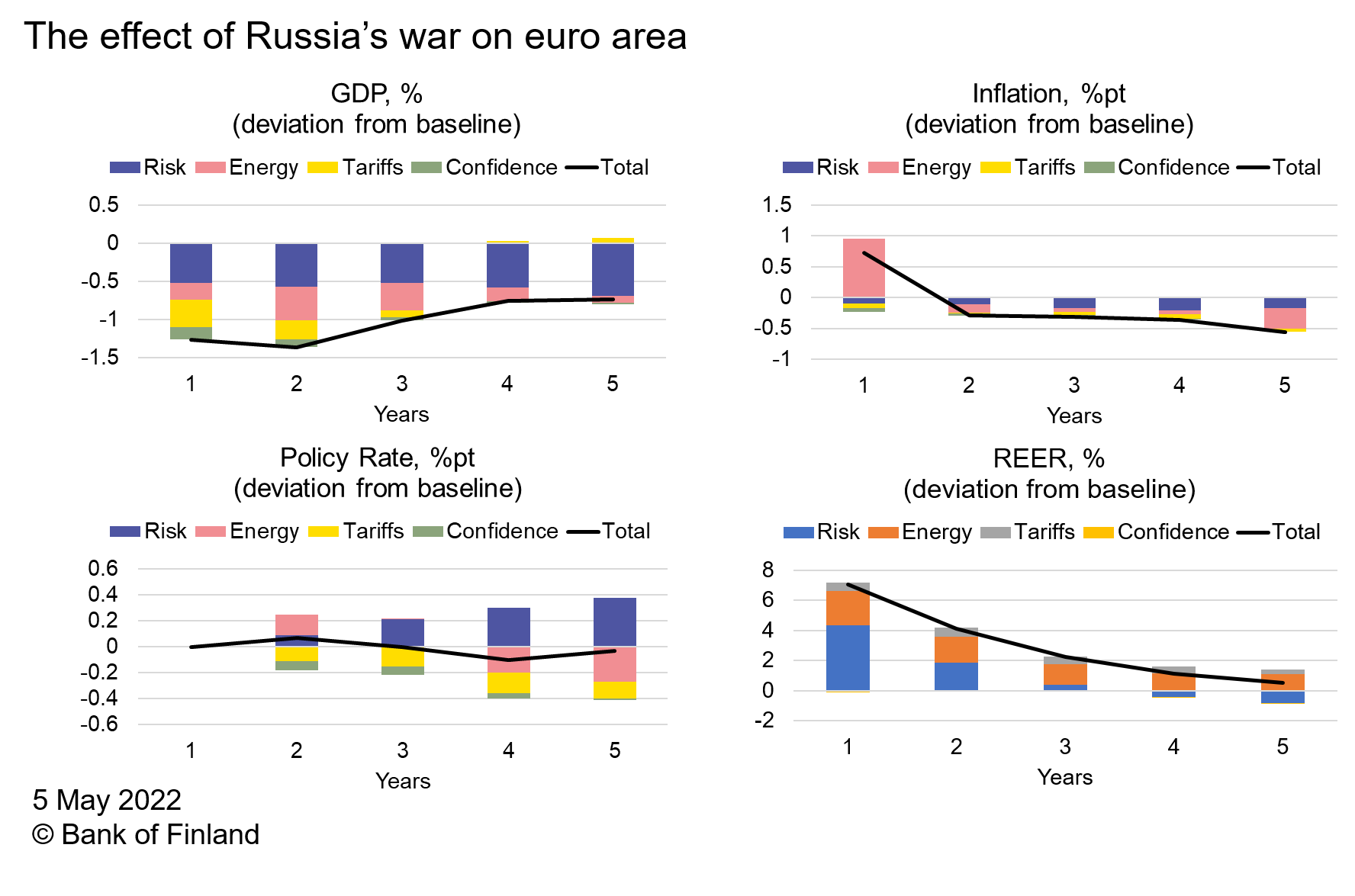

The effects of the Russia’s war on euro area inflation and growth are shown in Chart 4.

Chart 4.

Here, we see euro area GDP falls by about one percent in the short run. Inflation increases by slightly less that one percentage point in the first year and then returns to baseline. These results are well in line with analysis conducted by the ECB and OECD. The policy rate in the euro area is held constant for a year in the calculations before the ECB responds in the second year. This is a fairly bold assumption given the current inflation spike in the euro area. The euro depreciates about 7.5 percent in real effective terms.

3

Interpreting these results

Wars are humanitarian catastrophes with profound economic costs. Our modeling results suggest that everybody loses in this war, but the economic prospects for Russia are especially gloomy. As noted, we have not tried modeling the economic costs Ukraine might face. The economic fallout from Russia’s war is less pronounced in the euro area, but still substantial.

This modeling exercise may miss several crucial demand components for the euro area. Public investment (e.g. higher defense budgets) and increased investment in alternative energy sources can go up significantly in the short and medium term. These investments, or simply the expectation of such investments, could create growth momentum.

Our results are disheartening in the case of Russia’s economy. By initiating a brutal war against Ukraine, Russia has chosen to become much poorer and less influential in economic terms. Even in the short run, sanctions and Russia’s deteriorating economy constrain its ability to wage war and replenish the military manpower and materiel lost in Ukraine.

No comments:

Post a Comment